investing

-

Unlike us, financial institutions in developed countries use the KMV method of credit monitoring to determine the Expected Default Frequency (EDF). Since Merton, Black, and Scholes made revolutionary findings in financial theory, particularly in the mathematical valuation of options, it became clear that whenever an organization takes out a loan, it simultaneously buys a “default…

-

Do You Consider Default Risk When Purchasing Bonds on the Georgian Market? If So, How Specifically? There is an interesting metric called RORAC (Return on Risk Adjusted Capital), which was first used by Bankers Trust (acquired by Deutsche Bank in 1998) and later incorporated into the risk management systems of almost all major American and…

-

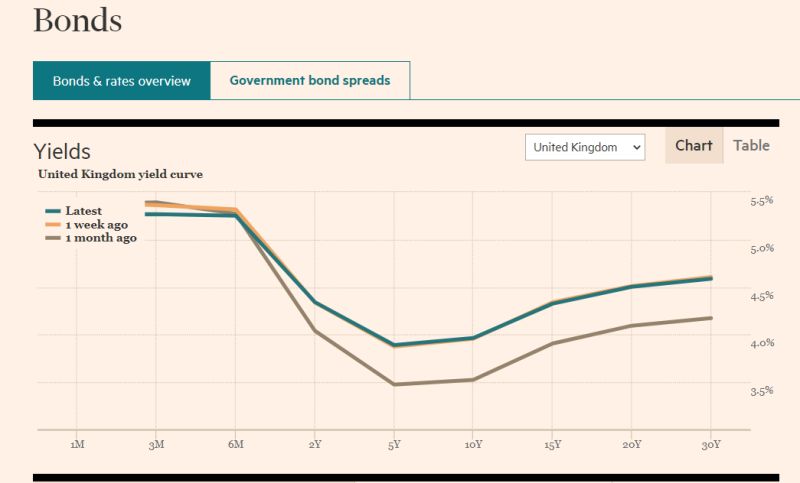

Factors Determining the Interest Rate on a Loan/Bond: i (j) = f (IP, RIR, DRPj, LRPj, SCPj, MPj) Where, Source: Financial Markets and Institutions – by A. Saunders, M. Cornett & O. Erhemjamts

-

Fisher Effect: The higher the inflation expectations, the greater the pressure on the securities market. Fisher Formula:i = (RIR + Expected-IP) + (RIR*Expected (IP)). Intuitively: The level of nominal interest rates approximately equals the real rate plus inflation expectations (the second part of the formula is a very small number). P.S.The graph shows the correlation…

-

Default Risk: DRP = Ji – Ti Default or credit risk is the risk that the payer will delay or fail to pay the tranche (interest or principal) within the agreed timeframe. The higher this risk, the greater the premium the market demands for the risk. Consequently, the risk premium (DRP) is the difference between…

-

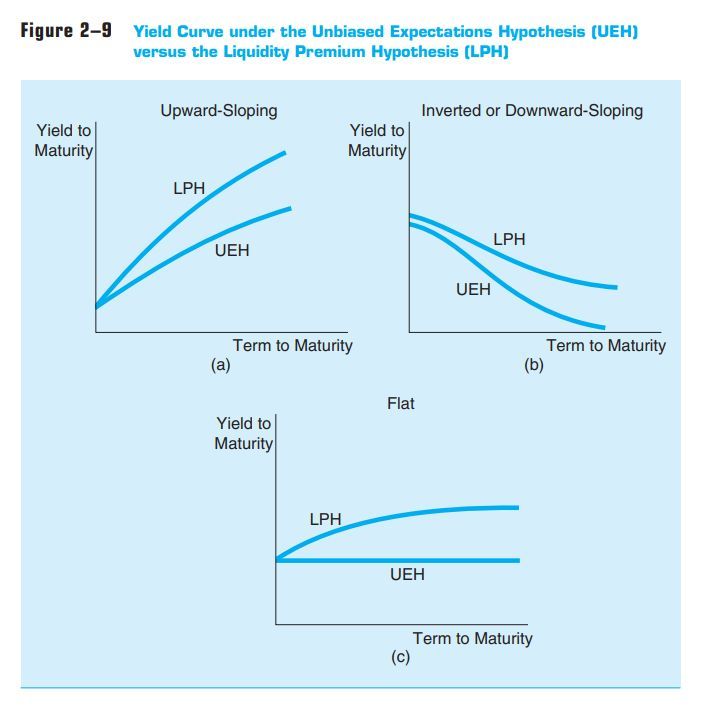

Unbiased Expectations Theory – What are the market’s expectations regarding interest rates? The Unbiased Expectations Theory essentially states that long-term interest rates are determined by the expected short-term interest rates for each subsequent period. The intuitive reasoning is as follows: if an investor expects that interest rates on one-year bonds will increase in each subsequent…

-

#liquidity risk premium & #unbiased expectations hypothesis. Money can be discussed as a negative NPV asset because it does not yield interest income, while on the other hand, it can be discussed as an option on positive NPV investment or as a hedge against adverse movements in cash flows. Consequently, there always exists some optimal…