VC Valuation

-

From the perspective of evaluating innovative projects, the model for releasing a new drug is very interesting. The process is fully regulated by the government, as neither the government nor businesses have an interest in thoughtlessly wasting such expenses or releasing inadequate drugs. The process consists of four stages, each with clearly defined goals and…

-

The valuation of real options can be approached in the same way as financial options, though the main issue here is finding the correct discount rate. To remind you, real options involve decisions that are irreversible or nearly irreversible, such as: What’s interesting here: A decision tree of events and choices is used to understand…

-

The term Pre & Post-money valuation used by venture investors often communicates inadequate numbers. Besides causing legal and tax-related issues, it also creates unrealistic expectations for Limited Partners. The issue lies in the fact that when calculated using a simple method, preferred and common stocks are equated, ignoring the value that the preferred stock gains…

-

Imagine offering startup employees an additional incentive: you’ll pay them another $5 million if they manage to increase the company’s value, which is currently $40 million, to $200 million. How would you assess the value of this additional incentive today? The offer mentioned above represents a Binary option, as the condition will either be met…

-

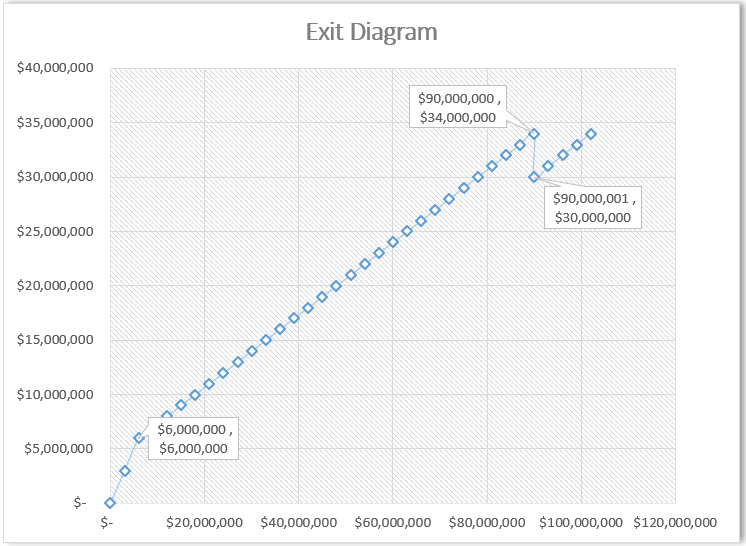

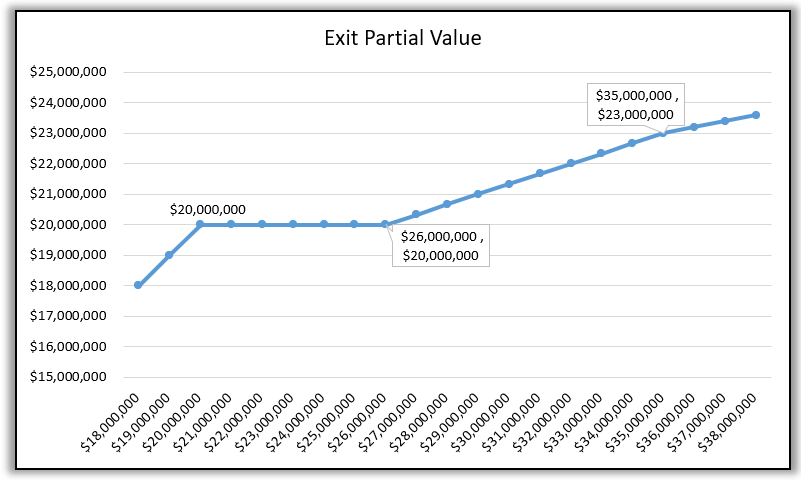

Formulas for valuing options tied to preferred investments become slightly more complex with each subsequent investment round. What needs to be considered here: Exit diagrams are naturally built based on the contracts with investors from previous rounds. Moreover, the math becomes even more complicated if we’re dealing with convertible shares across different rounds, since it’s…

-

The technique for valuing Random Expiration Callable Options (RE Calls) is used to assess the special conditions or options generated by a startup’s financing contract (link). Here, I will specifically discuss one example and upload the Excel model. The example examines a format of redeemable preferred (RP) shares, with versions including liquidity preference and additional…