Interest Rates

-

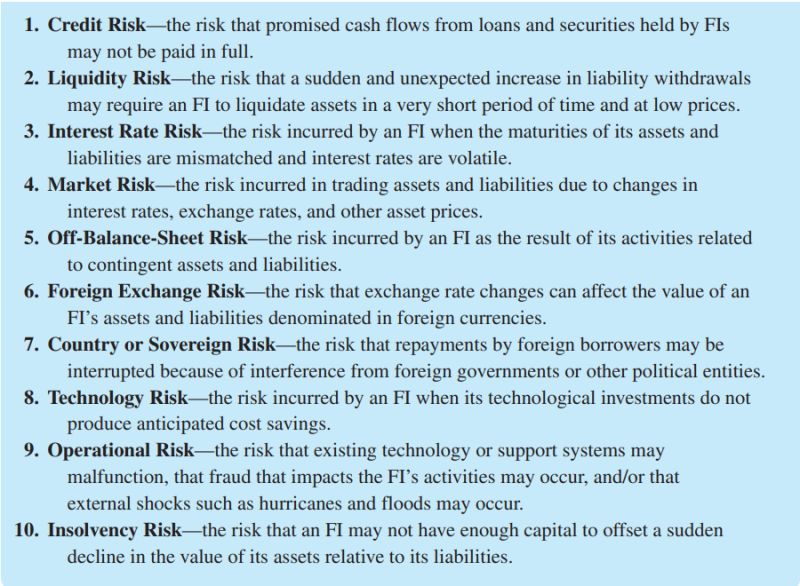

List of risks from the book – Financial Markets and Institutions – By Anthony Saunders, Marcia Cornett and Otgo Erhemjamts: Here’s the corrected list of risks from the image, starting with Credit Risk: Source: Financial Markets and Institutions – by A. Saunders, M. Cornett & O. Erhemjamts

-

Do You Consider Default Risk When Purchasing Bonds on the Georgian Market? If So, How Specifically? There is an interesting metric called RORAC (Return on Risk Adjusted Capital), which was first used by Bankers Trust (acquired by Deutsche Bank in 1998) and later incorporated into the risk management systems of almost all major American and…

-

Factors Determining the Interest Rate on a Loan/Bond: i (j) = f (IP, RIR, DRPj, LRPj, SCPj, MPj) Where, Source: Financial Markets and Institutions – by A. Saunders, M. Cornett & O. Erhemjamts

-

To assess the impact of interest rate risk on bonds and other fixed income assets, measures such as Duration, Modified Duration, Dollar Duration, Effective Duration, Convexity, and Portfolio Duration are used. (Macauley) Duration – Calculated by weighting the payment periods (in years) with the present values (PVs) of each expected tranche in the future. Ultimately,…

-

Fisher Effect: The higher the inflation expectations, the greater the pressure on the securities market. Fisher Formula:i = (RIR + Expected-IP) + (RIR*Expected (IP)). Intuitively: The level of nominal interest rates approximately equals the real rate plus inflation expectations (the second part of the formula is a very small number). P.S.The graph shows the correlation…

-

Default Risk: DRP = Ji – Ti Default or credit risk is the risk that the payer will delay or fail to pay the tranche (interest or principal) within the agreed timeframe. The higher this risk, the greater the premium the market demands for the risk. Consequently, the risk premium (DRP) is the difference between…

-

Unbiased Expectations Theory – What are the market’s expectations regarding interest rates? The Unbiased Expectations Theory essentially states that long-term interest rates are determined by the expected short-term interest rates for each subsequent period. The intuitive reasoning is as follows: if an investor expects that interest rates on one-year bonds will increase in each subsequent…