Interest Rates

-

#liquidity risk premium & #unbiased expectations hypothesis. Money can be discussed as a negative NPV asset because it does not yield interest income, while on the other hand, it can be discussed as an option on positive NPV investment or as a hedge against adverse movements in cash flows. Consequently, there always exists some optimal…

-

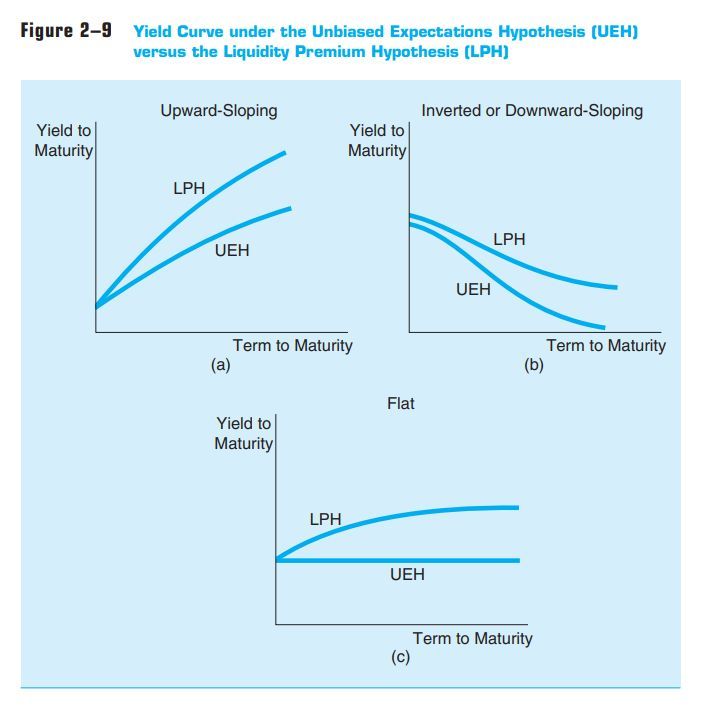

Directly affects the effectiveness of financial assets’ performance periods on interest rate movements. This moment is crucial because, despite the intuition that longer-term bonds are more sensitive to changes in interest rates, and therefore riskier and should have higher interest rates than short-term ones, in practice, the truth is not always so straightforward. Sometimes, the…

-

Market Segmentation Theory – This theory reflects the impact of events in different segments of financial markets on the relationship between interest rates and loan maturities. The theory posits that the market is divided into various segments, each with different preferences regarding bond maturities. For example, pension funds are more focused on long-term bonds, while…

-

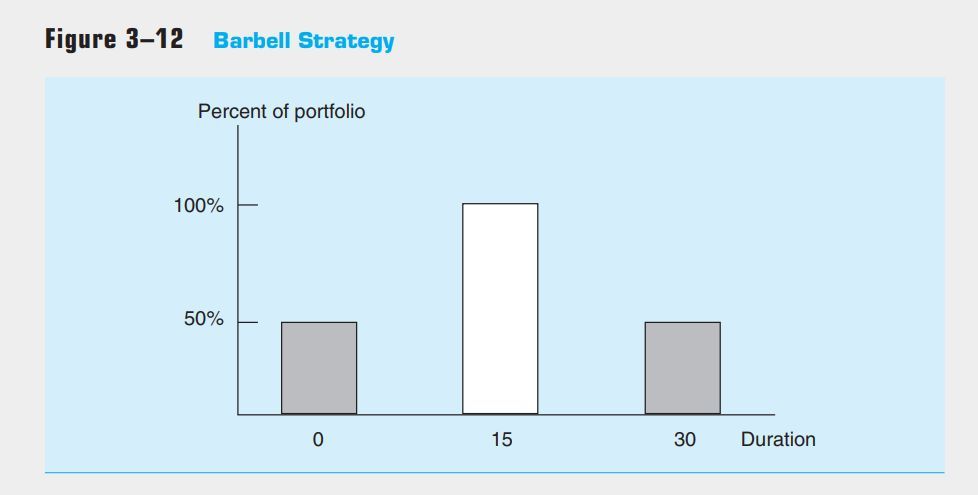

Convexity describes the curvature of the relationship between the price of an obligation and changes in interest rates. Consequently, it’s an important concept because, during interest rate fluctuations, capital losses are usually smaller than capital gains. In other words, the price decreases more for a given increase in interest rates than it increases for the…