Statement Reorganizations

-

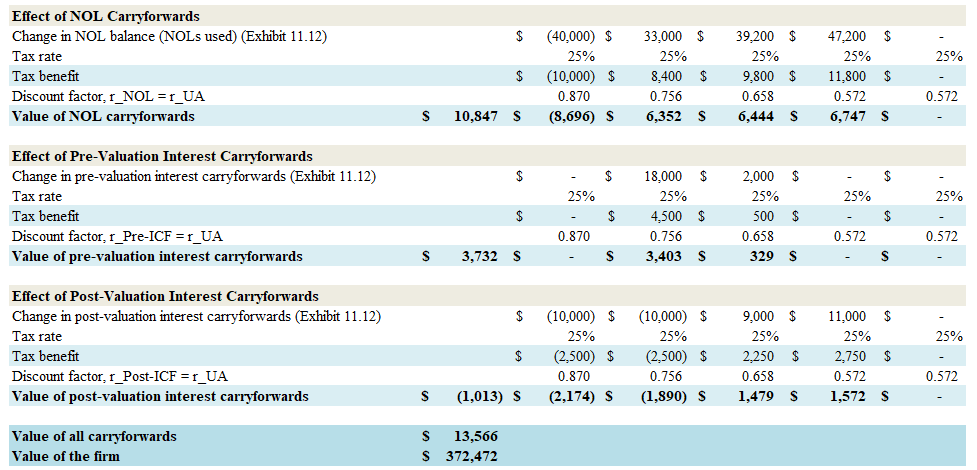

📌 An organization’s accumulated loss is an asset from a tax savings perspective, and should therefore be considered in valuation. 📊 Such an asset is divided into two parts: Net Operating Loss (NOL) and Interest Carryforwards… The latter arises in some countries’ tax legislation that regulates the limits for recognizing interest expenses for tax purposes.…

-

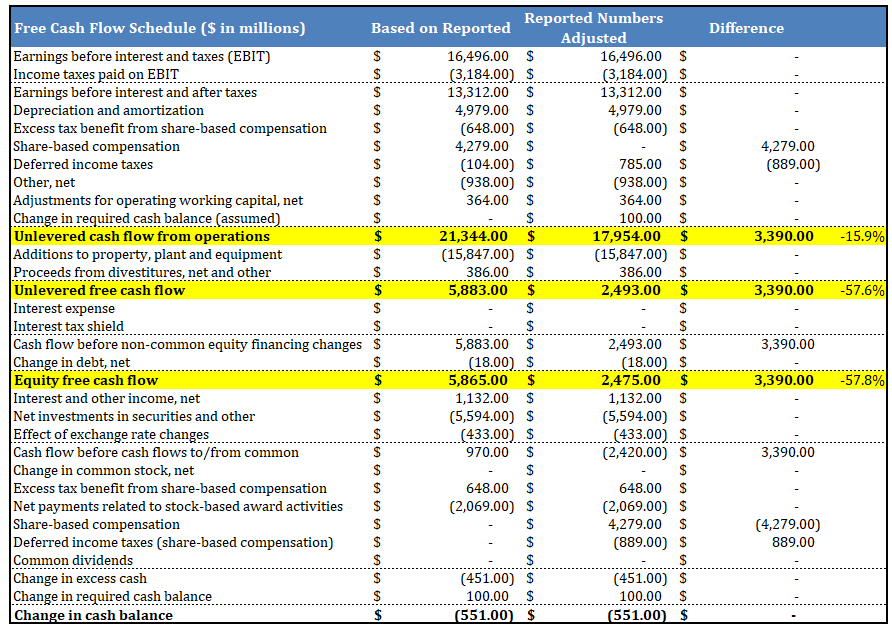

💼 Employee compensation tied to company capital is a widely used practice that sometimes significantly affects the organization’s Free Cash Flow and, consequently, its valuation. 📈 This refers to granting employees options or direct shares. Mistakes are easy to make because, in reported cash flow statements, this type of compensation often increases operating cash flow,…

-

The total value of an organization (EV) does not include operating liabilities, as there is no specific interest rate assigned to them. Therefore, these are considered in operating cash flows rather than the financing structure. Some liabilities are not explicitly operating or financial and depend on the evaluator’s perspective. For example, a lease can be…

-

Given that options are a crucial instrument both in the securities market and in strategic transactions, I will touch on a more complex but more realistic model for their valuation – the binomial method. In previous notes, I discussed two simple methods for option valuation (the portfolio replication and the risk-free world assumption methods). The…

-

To assess an organization’s value, we need to accurately measure the beta. Since the beta statistic for an individual organization is not reliable, we perform an industry beta analysis. This means we find similar companies, take their betas, unlever them, and then relever them according to the company’s leverage. This process is influenced by the…

-

According to financial legislation, intangible assets generated during the process of organic growth (including R&D) are not recorded on the balance sheet; instead, they are directly expensed, which distorts the true financial picture of the organization. Expensing R&D in the initial growth stages shows negative results, while in later stages it shows very high ROIC,…

-

In accordance with IFRS, almost every leasing contract exceeding one year is recognized as financial leasing. This implies that the contract’s capitalization should occur as assets and liabilities, while the lease payments should be split into amortization and interest expenses. Under GAAP, we encounter somewhat complex mechanisms. Here, the classification of leasing contracts happens as…