Investor Psychology

-

1. Second-Level Thinking Successful investing begins where obvious thinking ends. It is not enough to say that an asset, company, or market is good. The real question is what others already believe, what is already priced in, and what happens next if everyone reaches the same conclusion. 2. Understanding Market Efficiency (and Its Limitations) Markets…

-

💡 Pricing Power is a key indicator through which one can assess a company’s competitive position—and, accordingly, its intrinsic value. 🧠 Normative economics assumes that buyers are rational. But behavioral economics shows us that things aren’t that simple. Seen from this angle, here are some fascinating and unexpected insights: 🔹 Prestige Pricing – Sometimes, raising…

-

The most inefficient factory is the one where every machine and worker operates at full capacity…Yes, it’s counterintuitive. A stopped machine or idle worker should logically signal inefficient use of resources…But as the well-tested Theory of Constraints (ToC) teaches, reality is quite the opposite. ToC is discussed in all academic literature on operations management, but…

-

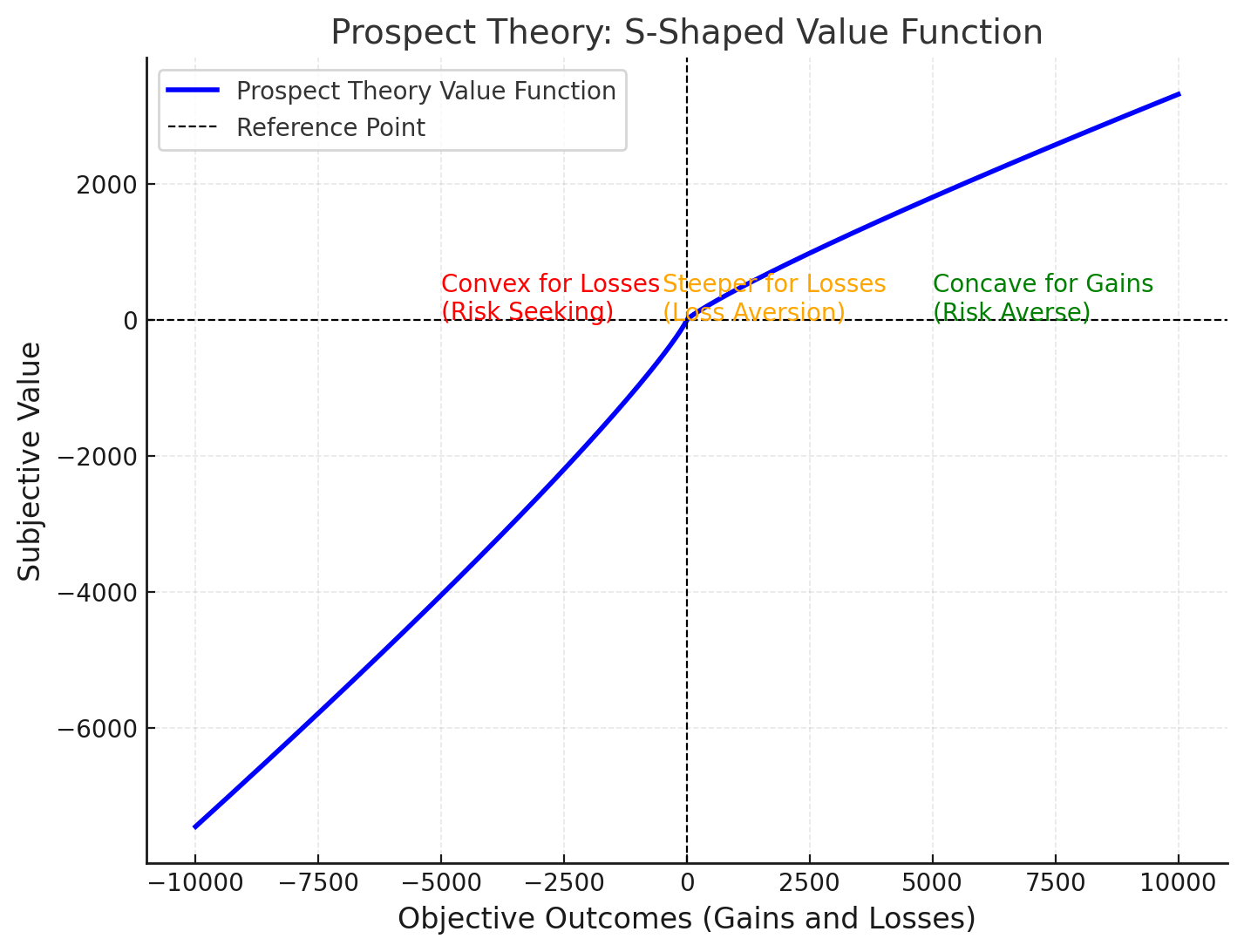

1. Bernoulli’s Utility Theory (Expected Utility Theory) Example: A person will prefer $10 for sure over a 50% chance of $20 because the utility of $10 is greater than the weighted utility of the risky gamble. This chart demonstrates how the expected utility of the gamble is calculated under Bernoulli’s Utility Theory: This approach visually…

-

Delays in construction projects and massive budget overruns appear to be not just a Georgian problem. Daniel Kahneman, in his book Thinking, Fast and Slow, refers to this phenomenon as the Planning Fallacy. The phenomenon arises from humans’ irrational tendency to plan for the desired (rather than objectively expected) scenario. Unfortunately, this issue affects all…

-

Among investors in the securities market, there’s a saying: “Sell in May and go away.” Below is some supporting data, but what causes this? The chart below shows the same type of statistics by sector. Notice that the retail sector is the least affected by this phenomenon: Perhaps it’s simply because more people take vacations…

-

Representativeness can heavily influence investor decisions and analyst forecasts. This cognitive bias leads us to assume that past performance will persist, making it a common source of error in growth rate estimation.Consider this example, shown in the chart below: 1️⃣ Initial Growth Expectations:Analysts build portfolios based on long-term earnings growth forecasts. The first two bar…