DCF Valuation

-

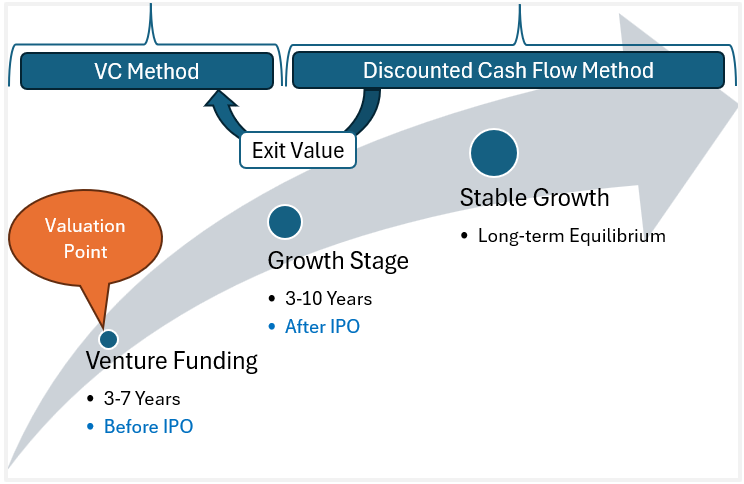

The use of the Venture Capital (VC) method for valuing an organization begins with determining the Exit Valuation, i.e., the value that the organization is expected to have when the fund successfully exits (either through an IPO or a sale to a PE fund). There are two approaches here: using the multiples method (comparative) or…

-

The table outlines the breakdown of the organization’s value into various components. This is the same as the economic balance. To determine the fair price per share, we need to add surplus assets to the core business value, subtract non-operational liabilities, and divide the result by the number of shares. It is not easy to…

-

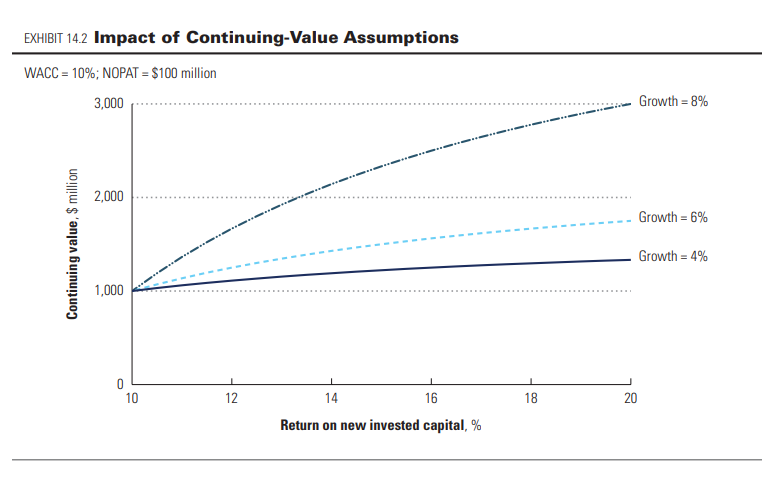

Simplifying horizon forecasts with formulas also imposes some limitations. Such situations are visible in photos, how forecasts are made under uncertain conditions for ROIC. Assuming ROIC = WACC. In such a scenario, when substituting ROIC with WACC in the main formula, we get: CV = NOPAT [t+1]/ WACC It’s evident that if we use this…

-

Valuation in Innovative Organizations In highly innovative organizations, it is often thought that the entire value of the organization lies beyond the horizon, increasing uncertainty and skepticism about the valuation. However, it is possible to view the value from a different perspective, as illustrated in the photo. The second column shows a breakdown of the…

-

For calculating the value after the horizon, it’s necessary to explain the stability of financial indicators. What does this mean? NOPAT – must be normalized. This is the basic figure for subsequent projections. Therefore, inadequately high or low figures here can lead to significant errors. The final forecast year’s NOPAT should be based on normalized…

-

Valuation Breakdown by Time Periods When breaking down an organization’s value into near-term and long-term components, the proportion of these two parts varies across different sectors. However, the weight of the value beyond the forecast horizon is significantly larger in any case (see photo). First Forecast Period The initial forecast period should ideally span 10-15…

-

Reorganizing the Profit and Loss Statement for NOPAT Calculation Just as the balance sheet is reorganized to calculate Invested Capital, the profit and loss statement is reorganized to calculate NOPAT. McKinsey recommends organizing the operational part of the profit and loss statement at the EBITA level, not at EBITDA or EBIT (see table). Why? EBITDA…