WACC, CoC, Structure

-

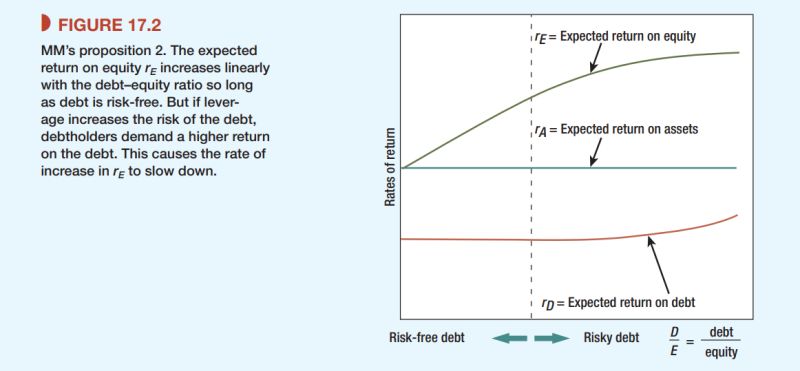

The beauty of the Modigliani-Miller (M&M) Theorem on the Irrelevance of Capital Structure lies in its ability to clarify investment and financial decisions. The theorem consists of two propositions: rE = rA + (rA − rD)*D/E From the second proposition, it follows that the discount rate used in valuing an organization is not dependent on…

-

თქვენს კომპანიას ფინანსური ლევერეჯის სტრატეგია აქვს? იცით როგორია თქვენთვის ოპტიმალური D/E კვეთა? M&M თეორია ამბობს, რომ მნიშვნელობა არ აქვს ლევერეჯის დონეს, ორგანიზაციის ფასი რეალური აქტივების ღირებულებით განისაზღვრება. ინტუიციური ლოგიკა ასეთია. სესხი უფრო იაფია ვიდრე აქციების გამოშვება, ამიტომ სესხის წონის გაზრდამ მოგება უნდა გაზარდოს ერთ აქციაზე. კი მოგება იზრდება, მაგრამ რისკიც იზრდება და შესაბამისად CoE იზრდება.…

-

The Dividend Irrelevance Theory (Franco Modigliani and Merton Miller, 1961) is one of the fundamental models that every investor should know. The theory states that it does not matter whether an organization distributes dividends or not; the dividend distribution policy does not affect the stock price. Mathematically, this holds true (if we disregard taxes). When…

-

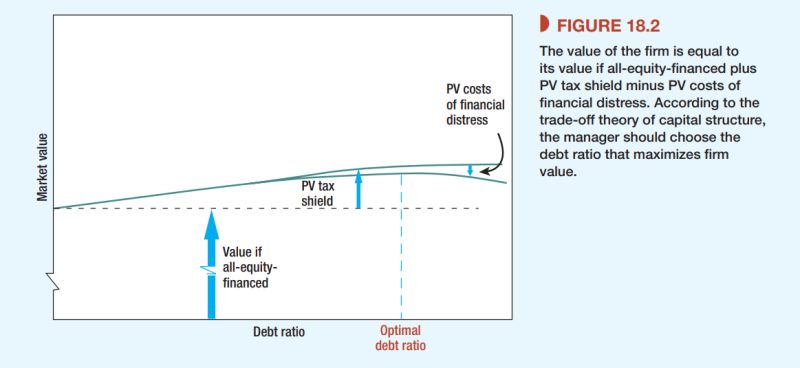

რატომ უნდა მოერიდოთ აქციების ყიდვას კაპიტალ-ინტენსიურ კომპანიებში? Pecking Order Theory… თუ ფინანსური ლევერეჯის ოპტიმიზაციის თეორია (Trade-of Theory) პრაქტიკაში მუშაობს, მაშინ რატომ არ ცდილობენ მენეჯერები მიზნობრივი ლევერეჯის მიმართულებით სვლას? რატომ განსხვავდება ლევერეჯის დონეები ერთიდაიმავე ინდუსტრიაში მყოფ კორპორაციებში? საკენკის თანმიმდევრულობის თეორია (Pecking Order Theory) მენეჯერების ქცევას შემდეგნაირად ხსნის: თეორია ეყრდნობა ინფორმაციის “ასიმეტრიულობას” მენეჯერებსა და აქციონერებს შორის. მენეჯერებს…

-

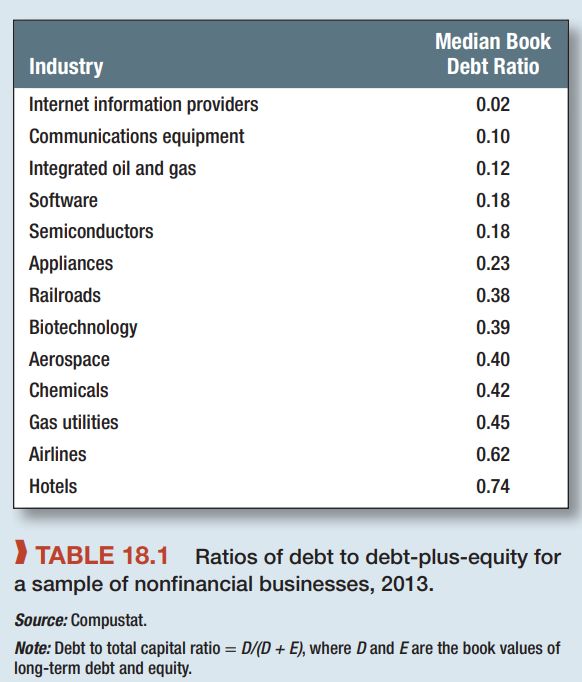

Can the Same WACC Be Used for Evaluating a Specific Project as for the Entire Organization? First of all, it’s important to note that smart investors more often use the industry’s WACC to evaluate an organization rather than the company’s own WACC, as average industry figures better reflect market risks and the optimal level of…

-

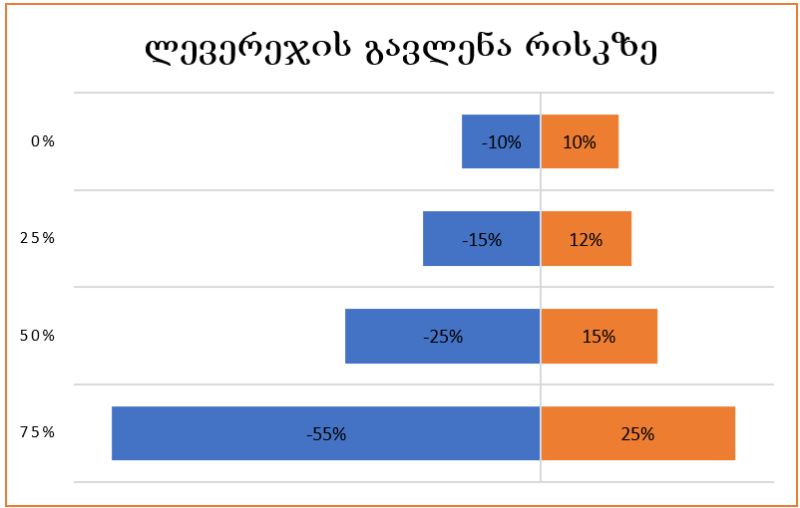

How Does Financing Structure Affect Risk? In essence, the financing structure does not impact the value of an organization. Value is created by the assets, and it doesn’t matter how the cash flows generated by these assets are distributed among the financing sources. Because the cost of debt is lower than the cost of equity,…

-

When discussing the evaluation of startups using the #VC method, one interesting point comes to mind: As I mentioned earlier, investment funds should provide an answer to the question of what happens to a startup when the fund exits? In the previous discussion, I mentioned that during evaluation, investors mainly rely on statistics of analogous…