Can the Same WACC Be Used for Evaluating a Specific Project as for the Entire Organization?

First of all, it’s important to note that smart investors more often use the industry’s WACC to evaluate an organization rather than the company’s own WACC, as average industry figures better reflect market risks and the optimal level of leverage.

Next, since WACC is directly and clearly influenced by the tax component, it varies with leverage. If the project to be evaluated is an average project within the organization, then it is advisable to use the same WACC, regardless of whether the project is financed with debt or equity. In this case, the company borrows against its overall assets and not just based on the specific project, whose leverage might change within the company in the short term.

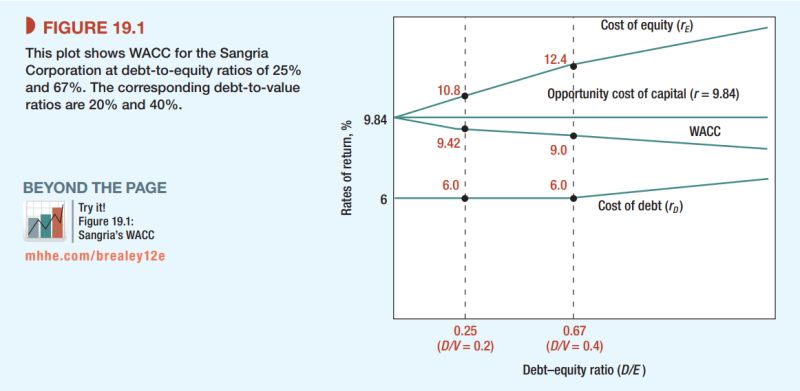

However, if the project’s systematic risks and leverage level are different in the long term from the typical activities of the organization, then the WACC should be adapted (as shown in the graph below). Here, simple formulas need to be used, which I will not delve into.

P.S.

There is the APV (Adjusted Present Value) approach. You can separately calculate the PV using the given WACC and discount all effects dependent on the financing structure (taxes, distress probability, asymmetric information) separately. This approach is often needed when projects are developed in different countries and conditions.

In the US, you can find leverage and WACC figures by industry at this link (however, it is not advisable to directly apply these figures in Georgia due to country risk – this is a separate topic).

https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/wacc.html

Source of photos and opinions:

Principles of Corporate Finance – by F. Allen, R. A. Brealey, & S. Myers