Cross-Border Valuation

-

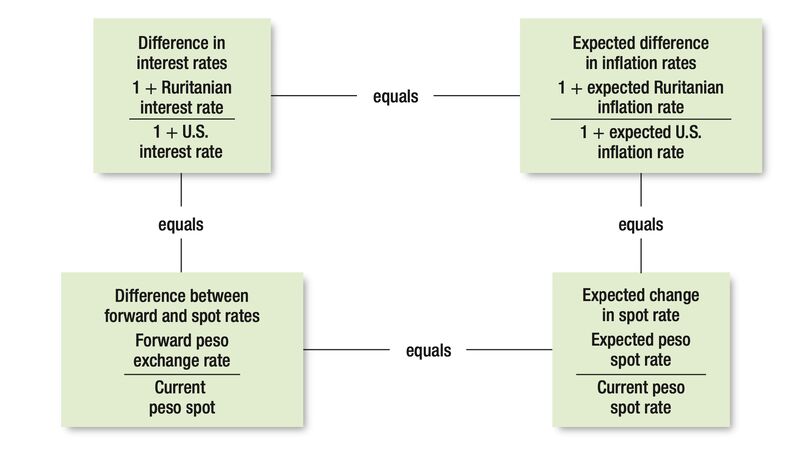

When evaluating investments outside, two approaches are used: 1. Forecasting is done by the investor in the organization’s base currency or 2. Forecasting is done in the target country’s currency, and conversion occurs after discounting. The more common practice is the first, but both should yield the same result in valuation and have some nuances…

-

Sure, here’s the translation in English: During project evaluations, a common error often occurs when incorrectly assessing the present value of selected capital, which is heavily dependent on various significant factors and one currency is mistakenly applied… In reality, the problem arises from the fact that the monetary parts of local projects are tied to…

-

Evaluating organizations operating in developing countries is associated with certain difficulties, and in this area, academics and practitioners often do not agree. The issue is that developing markets are characterized by additional systemic and specific risks. Often, an additional 3%-5% country risk is added to an organization’s WACC, which is a significant mistake. According to…

-

Sometimes, the financial statements of a subsidiary are translated into the parent company’s currency before being presented, which complicates the evaluation of the subsidiary. In such cases, it’s important to understand the translation principles used. See the table for GAAP and IFRS guidelines: When inflation is not high, both systems use the current method. This…

-

High inflation erodes the value of an organization because passing inflationary pressure onto customers is challenging and often not initiated – managers often do not realize the impact of inflation on value and do not try to raise prices adequately. The chart shows three scenarios for cash flow generation, assuming the organization does not experience…

-

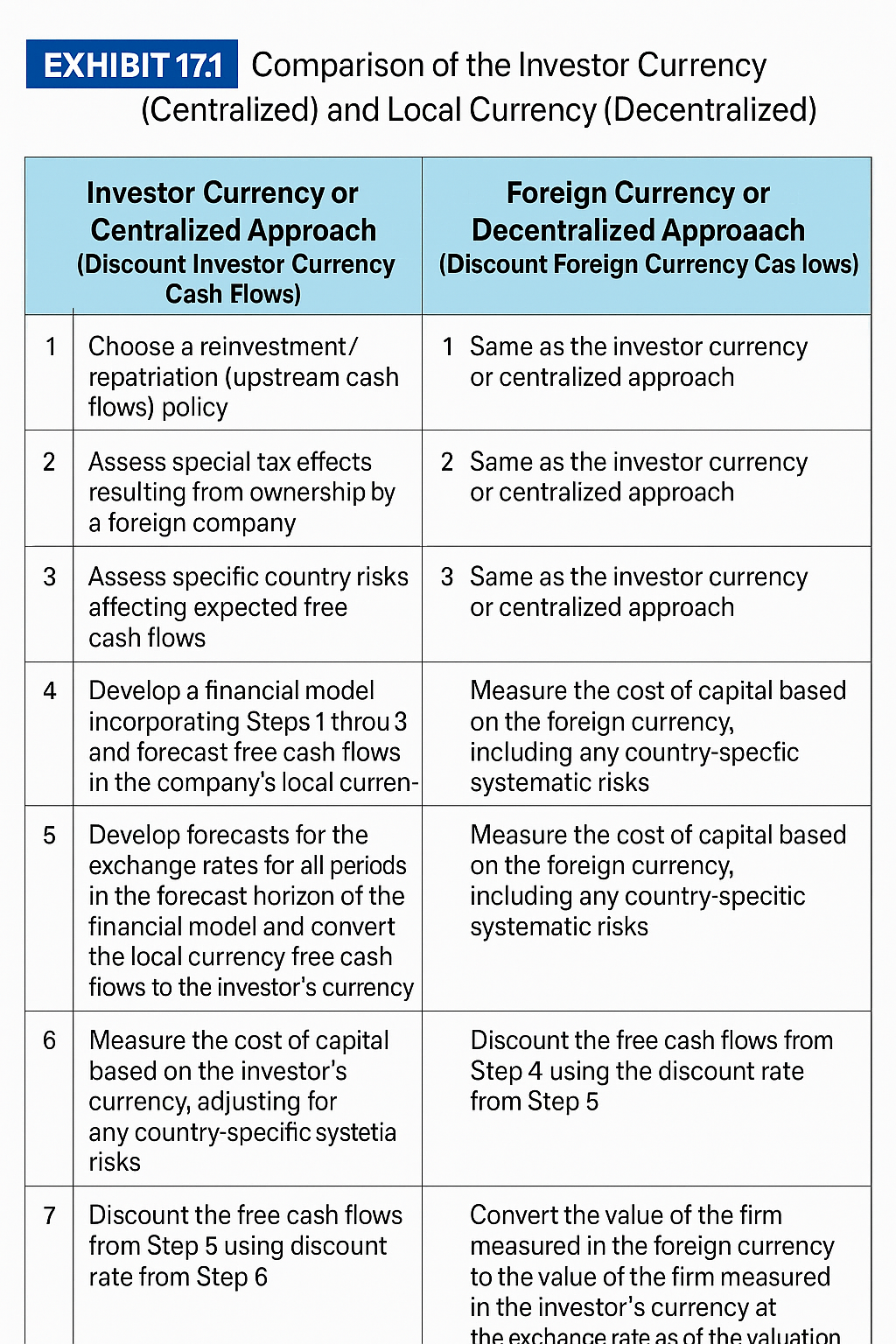

Subsidiary companies operating in another country use the local currency. Therefore, their evaluation requires special considerations. In this entry, I will discuss forecasting cash flows for a subsidiary company operating in another country. There are two approaches: Regardless of which method is used, the final result should be the same. To achieve the same result…

-

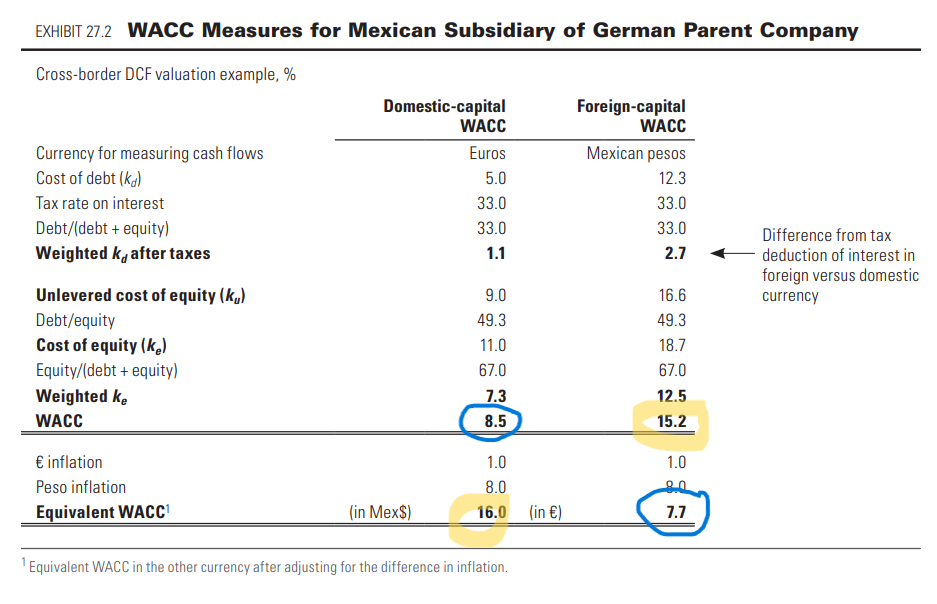

When discounting cross-border cash flows, several questions arise: which country’s cost of capital should be used? In which currency? And how should the beta of a subsidiary company be determined? Firstly, it is essential to consider the tax situation. There are instances when taxation occurs according to the laws of the subsidiary company’s country, or…

-

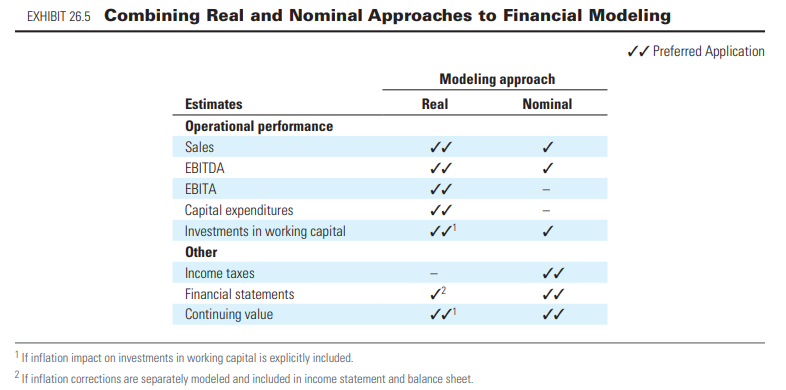

When inflation is very high, it becomes difficult to make forecasts in both real and nominal terms. Therefore, it becomes necessary to involve hybrid mechanisms. The table shows which version provides better results in relation to which item in the forecasts: We cannot make accurate tax forecasts with real figures because taxes depend on nominal…

You must be logged in to post a comment.