Derivatives

-

📌 Why Long-Term Stock Guarantees Are More Expensive Than They Look I recently came across a fascinating “Business Snapshot” in John Hull’s classic textbook Options, Futures, and Other Derivatives. It deals with a question many investors assume has an obvious answer: “If you invest for the long run, aren’t stocks guaranteed to outperform bonds?” Hull…

-

Microsoft was one of the first companies to grant stock options to all employees. Later it was estimated that thanks to this decision, more than 10,000 employees became millionaires. Stock-based compensation is still actively used today. It used to be even more popular because it helped attract valuable employees without appearing as an expense on…

-

How to Assess a Stock’s Risk Based on Historical Data We know that in finance, “risk” usually refers to volatility, i.e., uncertainty regarding changes. Here, I want to highlight a few important points. The volatility (σ) measure is very commonly used in practical finance when we: It is therefore important to understand clearly what this…

-

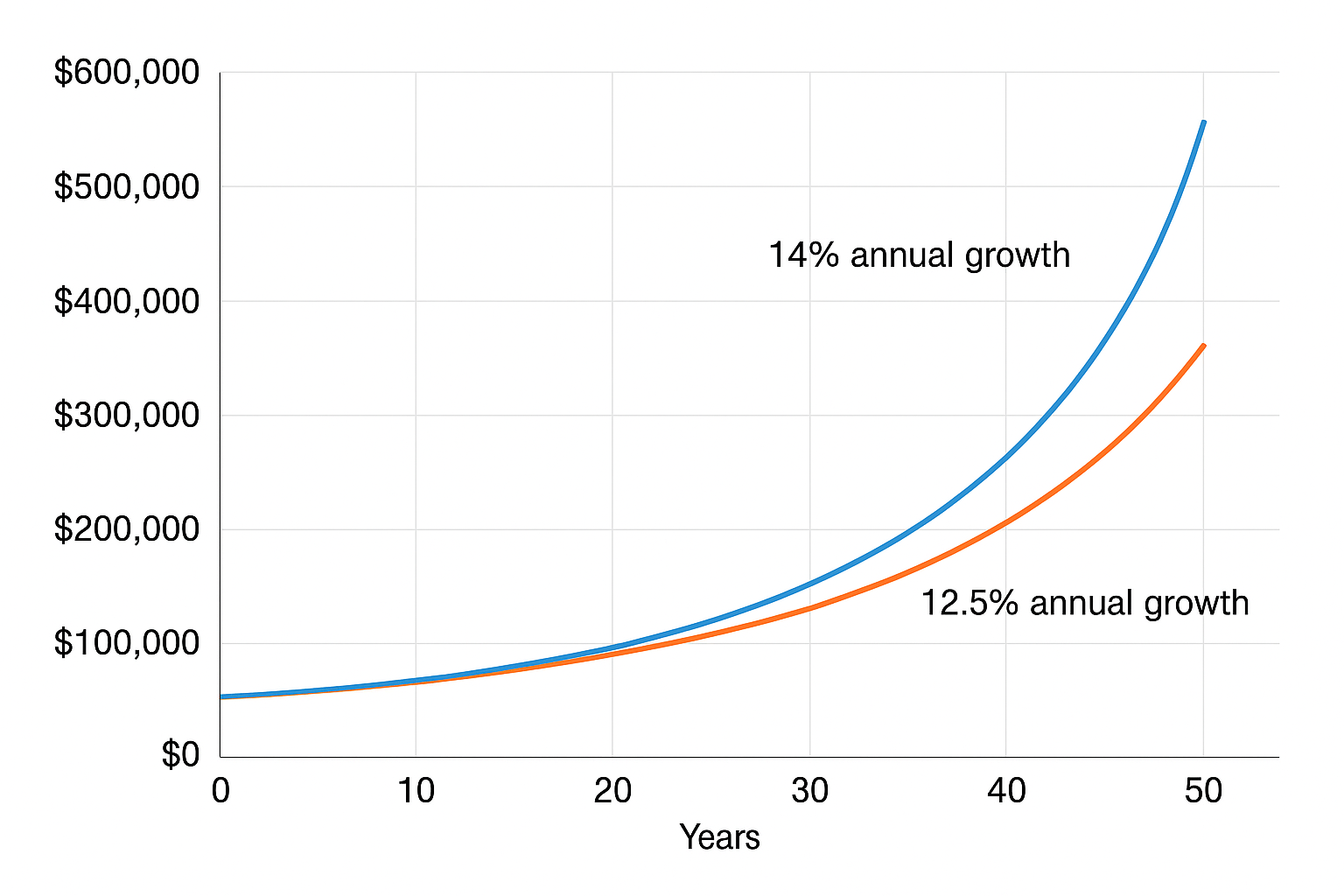

Suppose an investment fund (or a development company) promises you an average return of 14% per year. To convince you, they show that over the last 5 years their returns were: 15%, 20%, 30%, –20%, and 25%. The average of these is indeed 14%. Does the promise sound credible? Let’s check mathematically. The promise:A 5-year…

-

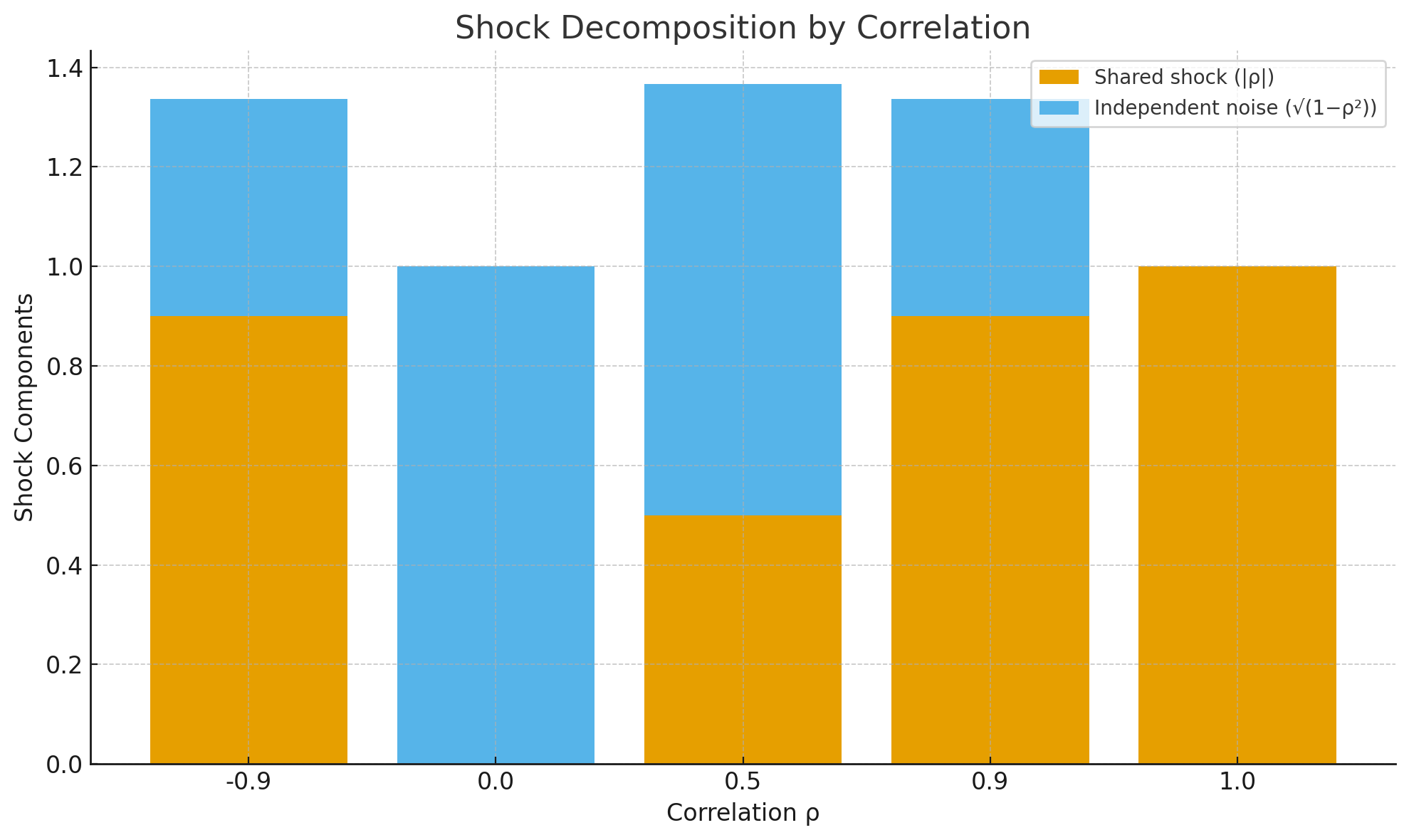

Why diversification fails during market crises… Assume two variables, (x_1) and (x_2), follow generalized Wiener processes: dx1 = a1·dt + b1·dz1 and dx2 = a2·dt + b2·dz2 The corresponding discrete–time versions of these continuous processes are: Δx1=a1*Δt+b1*ε1* √Δt და Δx=a2*Δt+b2*ε2* √Δt If we assume these processes are independent, then ε1 and ε2 are simply standard normal random…