Derivatives

-

If physicists use the Wiener process to describe the movement of molecules, for finance it is interesting because it helps us understand the price behavior of stocks and derivatives. A Wiener process is a specific version of a Markov stochastic process in which the expected value of the change is zero and the variance is…

-

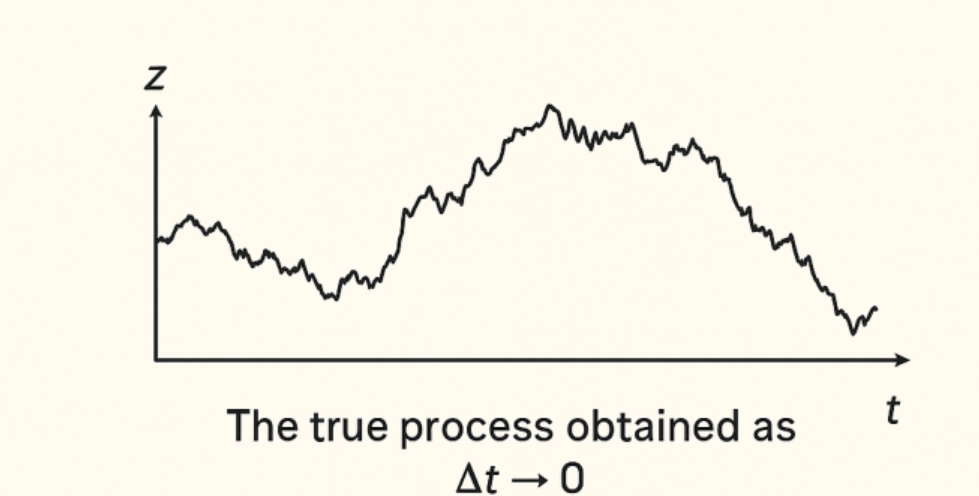

Why is uncertainty considered proportional to the square root of time (√t)? A Markov process (named after the Russian mathematician Andrey Markov (1856–1922)) is a special case of a stochastic process where, to predict a variable’s future value, only its current value matters. The past has no influence on the probability of future outcomes. The…

-

🎲 Have you ever noticed how life, business, and markets share one thing in common — uncertainty? Finance doesn’t ignore that; it embraces it.John Hull’s classic work on derivatives explains how we can actually model uncertainty — and that’s what this post is about. Let’s walk through it in plain words 👇 🌧️ 1. Stochastic…

-

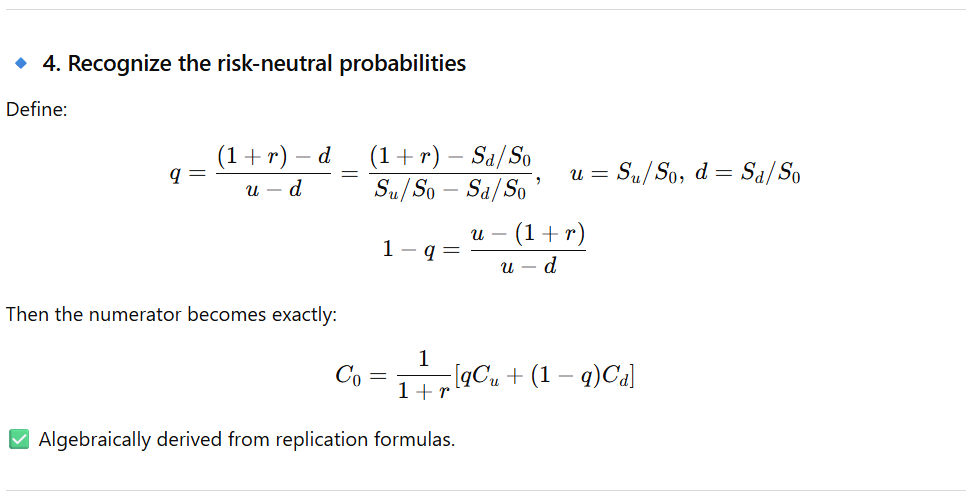

Using the Risk-Neutral Probability Method in Option Valuation is a bit counterintuitive. Why doesn’t the option price depend on the expected movement of the underlying stock — its probability of going up or down? Why does it not matter if the probability of the stock going up is 95% or 15%? Why do calculations done…