θ generally describes how an asset’s price depends on time — the time decay. When using formulas, it is important to pay attention to which θ is being discussed: an individual option, an option portfolio, or some other portfolio.

The good news is that when we are dealing with a portfolio of options written on a single underlying stock, θ is additive. At the same time, the θ of the underlying asset/stock is equal to zero.

For a portfolio, theta shows the range by which the value of the portfolio changes when time passes by a small amount.

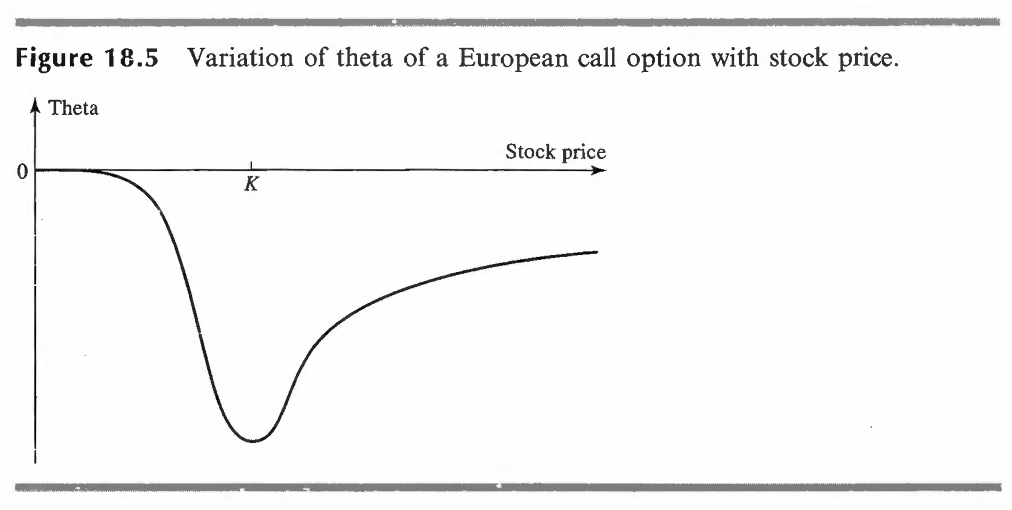

An option’s theta is negative because the expiration of the option has a negative effect on its value. However, in absolute value, it is larger when the stock price is closer to the option’s strike price, and it decreases as the stock price moves further away from the strike price.

The closer the option is to expiration, the smaller the influence of theta becomes.

Theta is not a target parameter for risk reduction, because there is no uncertainty associated with the passage of time, unlike with other Greeks. That is, portfolios are not specially adjusted to neutralize theta. However, it is included in formulas through which the gamma (Γ) parameter affects portfolio value, and from these formulas it follows that, within certain limits, theta is inversely related to gamma.

The theta of a non-dividend-paying stock option is calculated based on the Black–Scholes–Merton model.

See also this link — The Greek Letters

Source: Options, Futures & Other Derivatives, John C. Hull

Leave a Reply