Valuation of American-Style Futures Options using Binomial Trees

American-style futures options are valued using binomial trees. The difference between a futures option and a stock option is that exercising a futures option does not require an upfront payment to enter into the futures contract.

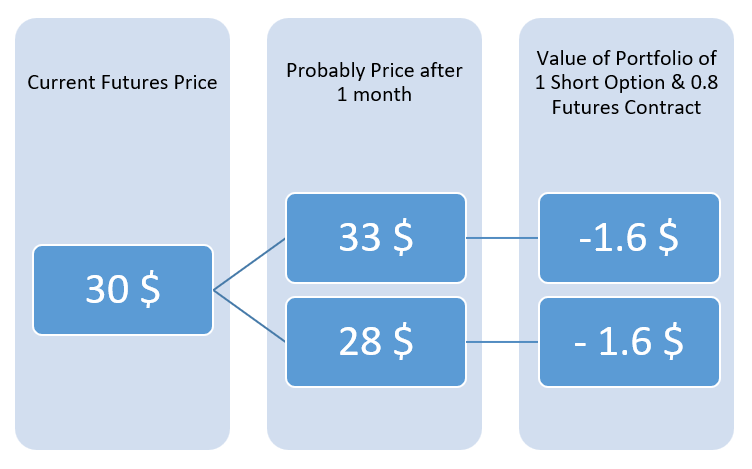

To illustrate with a simple one-step binomial tree, we first need to create a risk-neutral portfolio. This portfolio consists of a short position in one option and a long position of Δ futures contracts, where Δ (the hedge ratio) is chosen such that, regardless of whether the futures price goes up or down, the portfolio value remains the same.

For example, suppose we have the following data:

- One-step binomial alternatives: the futures price rises to $33 or falls to $28 in one month.

- Δ is calculated using the standard formula:

In our example, Δ = 0.8.

By taking Δ = 0.8 and assembling the portfolio accordingly, the portfolio value remains unchanged whether the futures price rises or falls.

Next, if we discount the portfolio value at the risk-free interest rate, we get – $1.59, which, considering that entering a futures contract costs nothing, implies that the option price today is $1.59.

Risk-Neutral Probability

The risk-neutral probability is a probability that ensures the portfolio has the same value in all future scenarios, as obtained by the formulas above.

To clarify, in the risk-neutral probability:

- The probability of a price increase is p

- The probability of a price decrease is 1 – p

p is calculated purely algebraically, so it can also be used as a shortcut to determine the option price.

In our case, p = 0.4, which results in an option price of $1.59.

Excel: Binomial Valuation of Futures Options model.

Note: The formula for p differs from the stock option case.

(Source: Options, Futures & Other Derivatives, John C. Hull)

Leave a Reply