Derivatives

-

The finite difference method, beyond finance, is actively used in physics and engineering fields, such as: The method involves breaking down a continuous differential equation into a system of finite difference equations and then solving them. In the case of option pricing, a matrix is created where one dimension represents the possible underlying asset prices…

-

The main advantage of the Monte Carlo simulation method over binomial trees is that it can be used to price options whose payoff depends not only on the underlying asset’s final price at expiration but also on the path it takes over time. For example, the payoff of Asian options is determined by the average…

-

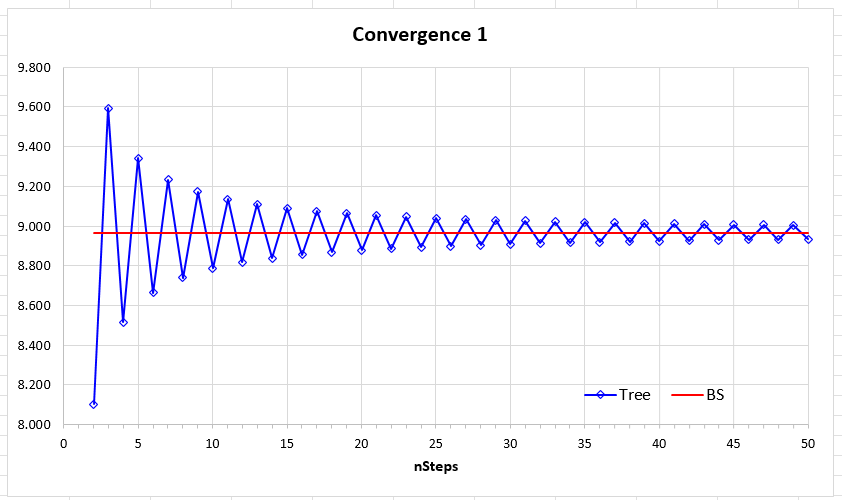

One method used to value an American option is the construction of a binomial tree. I have written about this before (Binomial Trees), so here I will focus on the more important nuances. Let us start with the Excel-based option calculator presented in John C. Hull’s book Options, Futures & Other Derivatives, which constructs binomial…

-

It turns out that the option price calculated using the Black–Scholes–Merton (BSM) model differs from the price formed in the real market. The reason is that the market perceives the volatility of the underlying asset as a function of the strike price and the option’s time to maturity. The graph shows the so-called volatility smile…

-

The presence of a risk-free asset portion in a portfolio can insure its value with almost the same precision as purchasing put options. The value of a diversified investment portfolio can be insured by buying a put option on the corresponding index (see in detail: Portfolio Insurance with Index Options). However, since a put option…

-

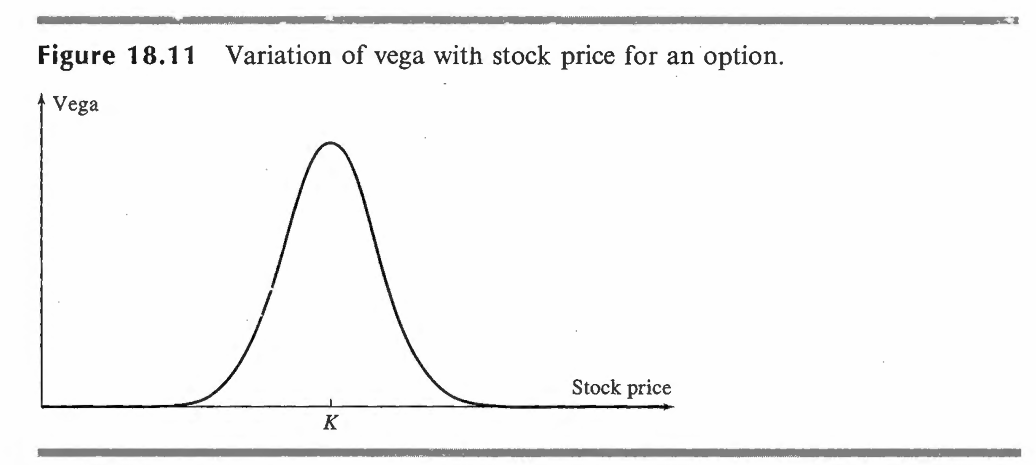

Here is a clear, accurate translation into English, keeping the financial meaning intact: Vega (V) Vega is the rate at which the value of an options portfolio changes in response to changes in the volatility of the underlying asset’s price. In other words, the larger the vega (whether positive or negative), the more sensitive the…