Here is a clear, accurate translation into English, keeping the financial meaning intact:

Vega (V)

Vega is the rate at which the value of an options portfolio changes in response to changes in the volatility of the underlying asset’s price. In other words, the larger the vega (whether positive or negative), the more sensitive the portfolio’s value is to changes in the volatility of the underlying asset (sensitivity to volatility).

A portfolio can be made vega neutral, just like with the other Greeks. This can be done by adding or removing options from the portfolio. If V is the portfolio’s Vega, and Vₜ is the Vega of a single option, then adding a position of −V / Vₜ options will make the portfolio Vega neutral.

An important point here is that a portfolio consisting of only one type of option cannot be simultaneously Gamma- and Vega-neutral. In such cases, it is necessary to hold at least two different types of options written on the same underlying asset.

Suppose we have the following portfolio:

The portfolio is delta neutral, but gamma and Vega create risks of loss in portfolio value. If we want the portfolio to become gamma and Vega neutral, we need to calculate the quantities of options that will achieve this. That is, we need to solve a system of equations:

From these equations, it follows that if we add 400 units of Option 1 and 6,000 units of Option 2, the portfolio becomes gamma and vega neutral. However, delta will change:

400 * 0.6 + 6,000 * 0.5 = 3,240

which means that 3,240 units of the underlying stock must be sold. This operation does not affect gamma or vega.

Vega calculation formula:

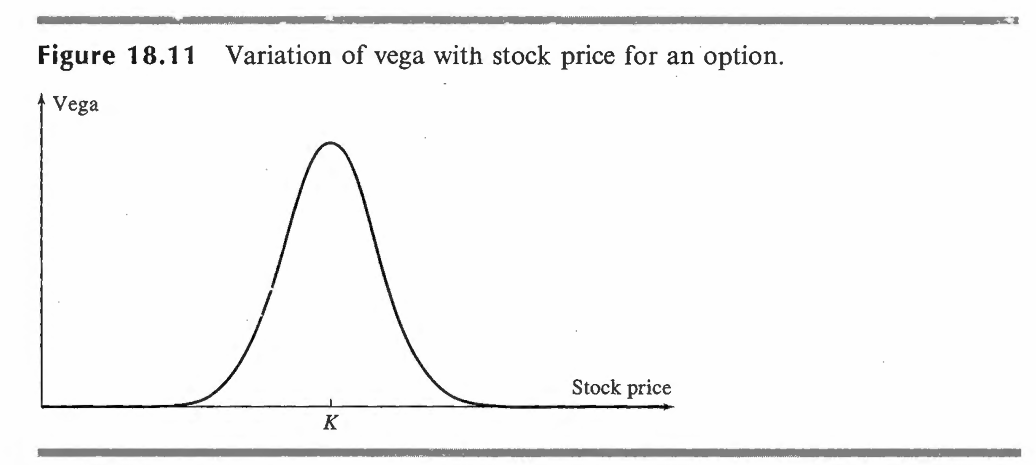

Finally, vega is highest when the stock price is closest to the option’s strike price.

Source: Options, Futures & Other Derivatives, John C. Hull

You must be logged in to post a comment.