Commercial Real Estate Analysis and Investments, D. M. Geltner, N. G. Miller, J. Clayton, P. Eichholtz

-

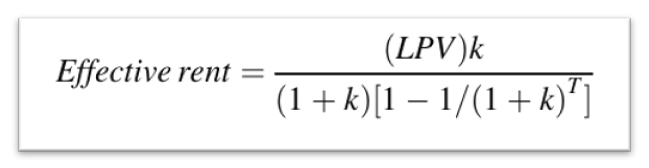

The term “effective rent” is used to evaluate and compare the profitability of leased real estate. In essence, it represents the present value of rental income, translated across time periods. It is a useful metric when we want to compare two lease offers with different terms, either from the landlord’s or tenant’s perspective. First, I…

-

Investments in real estate consist of various stages, and at each stage, both the risk and the corresponding expected return (Opportunity Cost of Capital) differ. Initially, risks are high, but as more investment is made, future forecasts become clearer and the level of risk decreases. Source: Commercial Real Estate Analysis and Investments, D. M. Geltner,…

-

It appears that option theory explains well why periodic overbuilding is both inevitable and, at the same time, rational. While other theories (e.g., the DiPasquale-Wheaton 4-Quadrant Diagram) often attribute oversupply to distorted behavioral and irrational actions, from the perspective of option theory, such behavior becomes sufficiently normative. Real and financial options differ in that real…

-

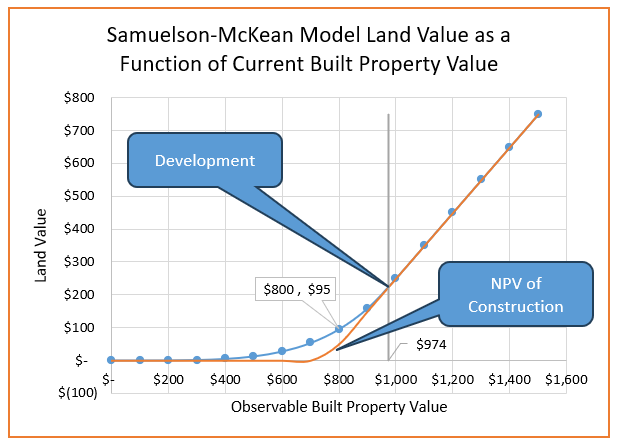

So when should land development actually occur? We know that postponing a project has value, just like an option, and this affects the price of land. Using a simplified real options approach, we can calculate the option premium from a one-year delay perspective. We can also make the model more complex, using binomial trees to…

-

Is it worth buying land for a development project if the business plan shows a negative NPV?The initial reaction is “no,” but the decision is not that simple. The point is that owning land comes with the option to delay the project in time—and that option has value. This component of land value is called…

-

Fixed-income assets come with default risk. For example, the default probability statistics for commercial mortgages by years since loan origination look like this: Source: Commercial Real Estate Analysis and Investments by D. M. Geltner, N. G. Miller, J. Clayton, P. Eichholtz In the event of default, it is often impossible to recover the full amount…

-

For a real estate investor, it’s important to understand how valuable a loan refinancing option is, which can be assessed using the Black-Scholes financial options pricing model. For example, on a $100,000, 10-year mortgage loan, the value of this option came out to be $32,600. This represents the value of the borrower’s asset, which is…