Risk

-

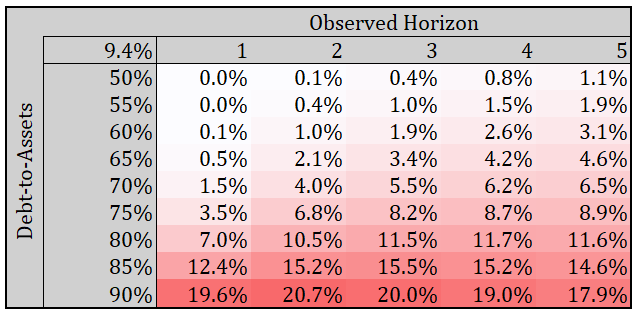

💬 How to Estimate Cost of Debt for Private Companies? For “listed” companies, the Cost of Debt (CoD) is more or less accessible. But how do we estimate this number when valuing a private company? Let’s say a company has a loan at 8% — can we just say its CoD is 8%?Or imagine the…

-

How to Calculate Expected Default Loss on a Bond? The cost of debt is often confused with the yield to maturity (YTM) of a bond/loan. The promised return is equal to the cost of debt when there is no risk of default. However, because there is a real risk of default, we must discount the…

-

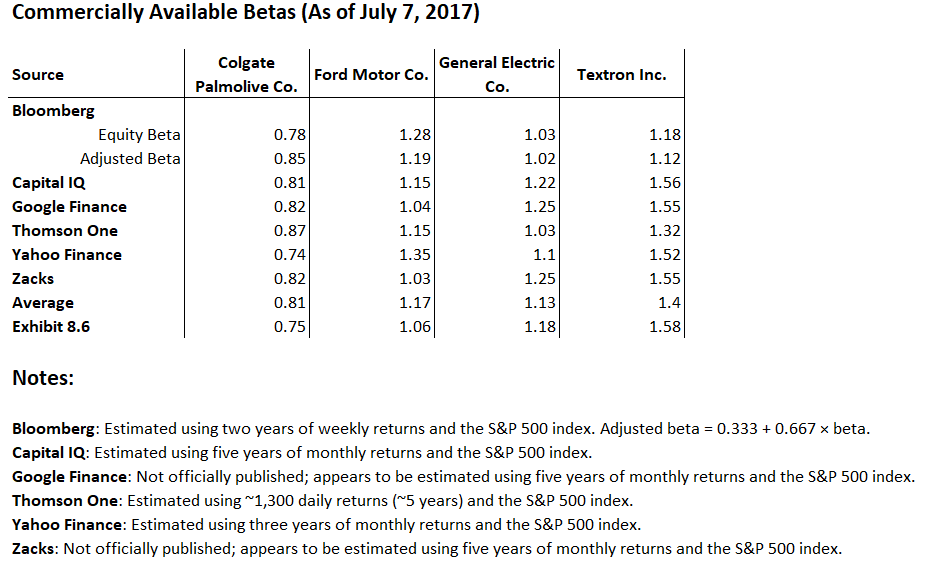

Adjusted β – It’s important to understand that statistical analysis provides an approximate rather than a “true” beta. Different commercial sources (as shown in the table) provide different data because they rely on different assumptions. The differences in assumptions pertain to the time frame over which beta is calculated (e.g., month) and the total period…

-

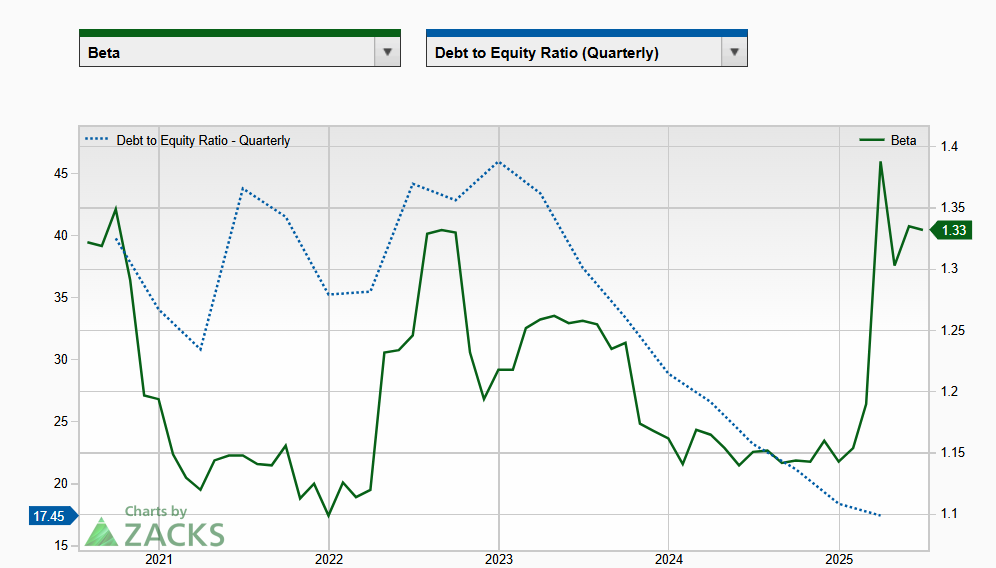

An organization’s capital (#equity) is subject to systemic risk related to industry cyclicality, operational leverage, and financial leverage… The most significant impact on this uncertainty is seen in management decision-making and financial policy… Therefore, when assessing discounted cash flows for valuation, we should consider whether the organization’s financial policy has significantly changed… For instance, Amazon’s…

-

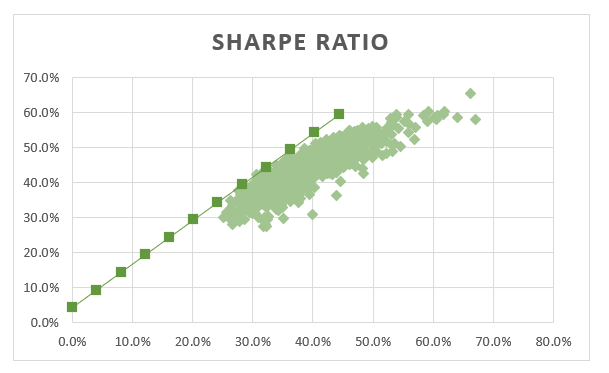

It is generally believed that an investment portfolio is better constructed the higher its Sharpe ratio (Sharpe Ratio – William F. Sharpe). The Sharpe ratio describes the relationship between a portfolio’s risk premium and its risk: Sharpe Ratio = Risk Premium/Standard DeviationSharpe Ratio = (Return-Risk Free Rate) / δ Why is this interesting? In the…

-

In futures trading, both end-users of raw materials and traders participate.The first group aims to hedge their business margins, while the second seeks to profit from price fluctuations. However, there are cases where a transaction is perceived as a hedge, but in reality, it’s speculative—and carries significant risk. Below are three real-life scenarios that illustrate…