investing

-

What mistake might you make when replicating someone else’s portfolio? There’s a strong temptation to buy a stock that’s in a famous investor’s portfolio. Why not? Bill Ackman or Warren Buffett have vast experience, access to an ocean of resources for making the right decisions, and (let’s face it) there’s a high chance they might…

-

When we described the use of the VC method by venture funds to make investment decisions in a startup, the model was solely about the investment decision (VC Method). The next stage involves deciding in what format the investment will be made—whether it will be preferred shares, convertible preferred shares, or something else. When we…

-

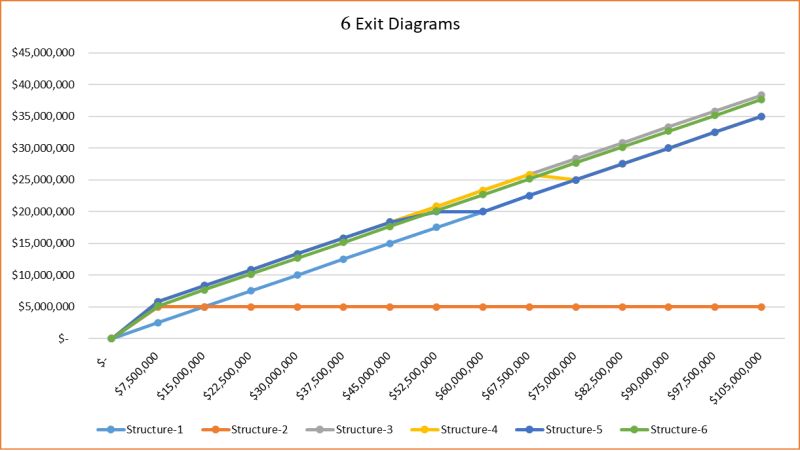

Venture capital funds primarily use preferred shares (redeemable, convertible, mandatorily convertible, automatically convertible, etc.) to finance startups. Based on the details of the agreement, exit diagrams are created, which show how profits/assets are divided in the event of liquidation or the fund’s exit. For example, the diagram below shows a simple exit diagram for convertible…

-

Value investing seems very simple – you buy a stock when it’s below its intrinsic value and sell it when it exceeds that intrinsic value. But in reality, making the right decisions is much more difficult, even if we could see the intrinsic value with mathematical precision and have better knowledge compared to the entire…

-

According to the M&M theory, the formula for unlevering and levering capital is straightforward, but there are variations of the formula adapted to different situations. Situations can vary based on two parameters: Similarly, the formulas change in the case of levering: Finally, the formulas also change when unlevering or levering beta: The corresponding Excel file…

-

It is evident from practice that in cyclical industries (aircraft, iron, paper, chemicals, real estate…) organizations periodically create excess capacity and cycle the industry. When selling prices are attractively high, business inertia takes over. At this time, all competitors are moving at high speed, and even rational executives find it difficult to convince shareholders that…

-

The text discusses the challenges and methods involved in valuing financial institutions, particularly banks, compared to corporations. Here’s an English translation: Valuing Banks: It is considered that evaluating financial institutions, including banks, is a more complex task than evaluating corporations. Banks are characterized by high and variable financial leverage. Their published reports do not truly…

-

Evaluating organizations operating in developing countries is associated with certain difficulties, and in this area, academics and practitioners often do not agree. The issue is that developing markets are characterized by additional systemic and specific risks. Often, an additional 3%-5% country risk is added to an organization’s WACC, which is a significant mistake. According to…

-

The optimal level of financial leverage is determined, on the one hand, by the amount of tax savings an organization receives by deducting interest expenses, and on the other hand, by the magnitude of the probabilistic costs of bankruptcy arising from increased risks. However, one component that I haven’t encountered in academic literature but have…

You must be logged in to post a comment.