Advanced Issues

-

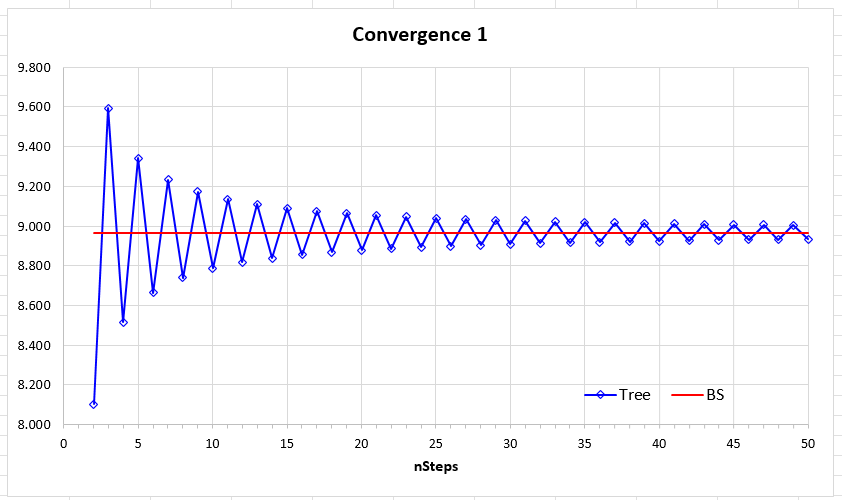

One method used to value an American option is the construction of a binomial tree. I have written about this before (Binomial Trees), so here I will focus on the more important nuances. Let us start with the Excel-based option calculator presented in John C. Hull’s book Options, Futures & Other Derivatives, which constructs binomial…

-

It turns out that the option price calculated using the Black–Scholes–Merton (BSM) model differs from the price formed in the real market. The reason is that the market perceives the volatility of the underlying asset as a function of the strike price and the option’s time to maturity. The graph shows the so-called volatility smile…

-

The presence of a risk-free asset portion in a portfolio can insure its value with almost the same precision as purchasing put options. The value of a diversified investment portfolio can be insured by buying a put option on the corresponding index (see in detail: Portfolio Insurance with Index Options). However, since a put option…

-

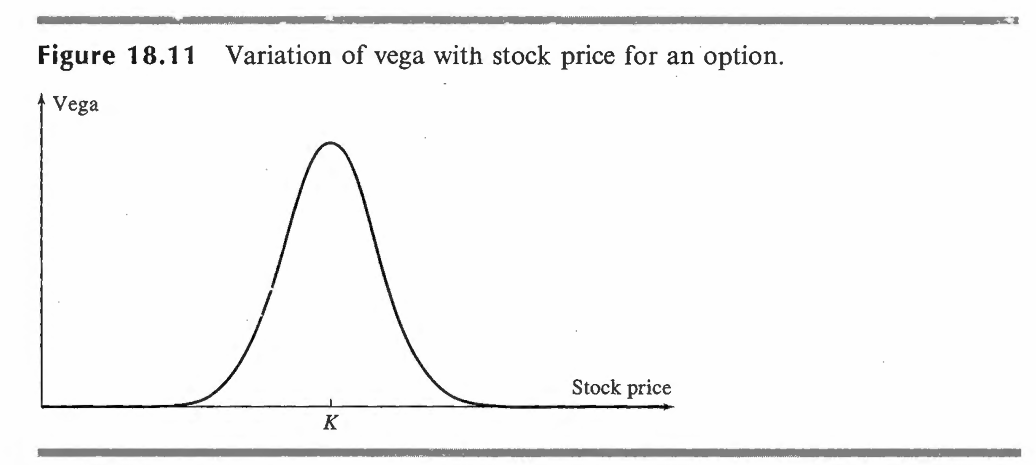

Here is a clear, accurate translation into English, keeping the financial meaning intact: Vega (V) Vega is the rate at which the value of an options portfolio changes in response to changes in the volatility of the underlying asset’s price. In other words, the larger the vega (whether positive or negative), the more sensitive the…

-

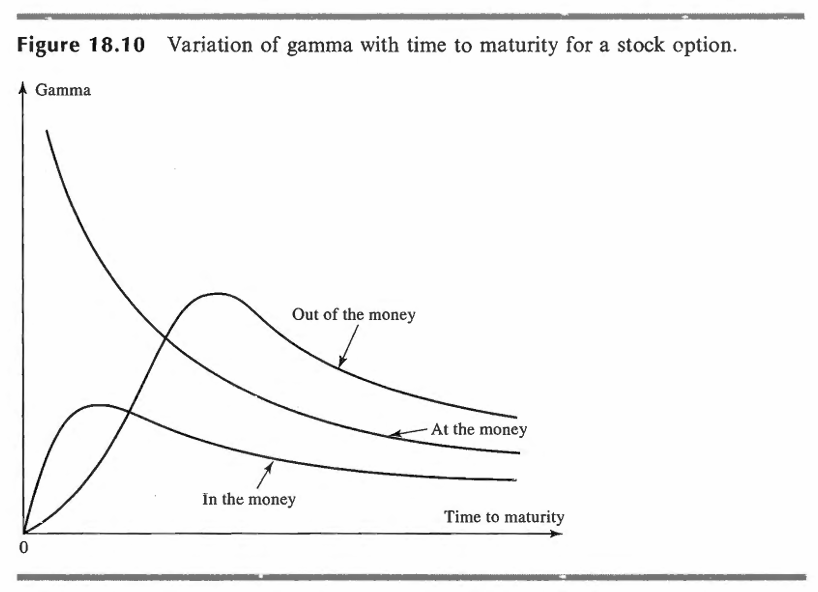

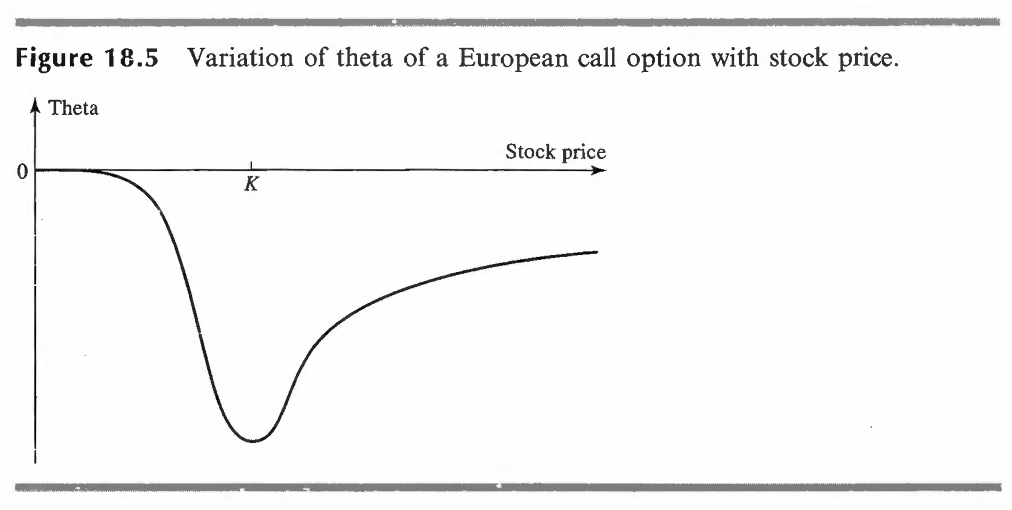

Also, the relationship between the option price and the underlying price is not linear. Gamma determines the degree of curvature of this relationship. It is the second derivative that affects the option price’s sensitivity when the stock price changes over a wide range. (For small changes, delta is sufficient, because the curvature does not have…

-

Trading options requires risk hedging.Suppose an investment fund uses the Black-Scholes-Merton model to calculate the value of a call option and then sells it in the market at a higher price. In substance, it has made a profit, but this profit is not yet realized because the option has not expired. For example, let’s assume…

-

Black’s brilliant model was originally developed for pricing European futures options (“The Pricing of Commodity Contracts,” Journal of Financial Economics, 3 (March 1976)). Later, it turned out to be very convenient in practice for spot options as well. The main assumption of the model is that, in a risk-neutral world, futures prices evolve in the…

-

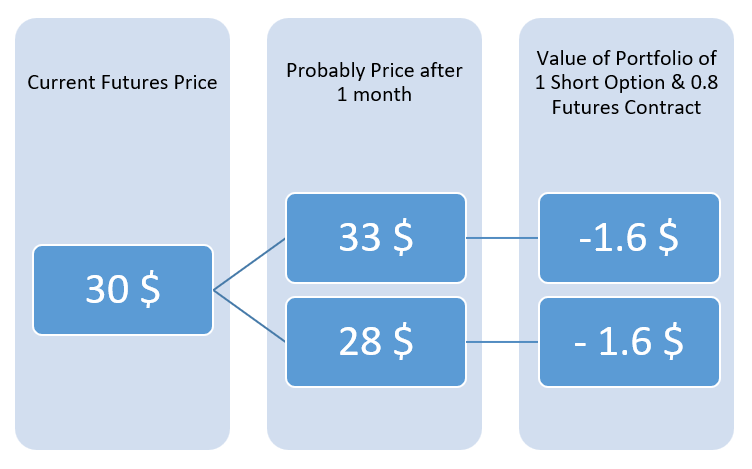

Valuation of American-Style Futures Options using Binomial Trees American-style futures options are valued using binomial trees. The difference between a futures option and a stock option is that exercising a futures option does not require an upfront payment to enter into the futures contract. To illustrate with a simple one-step binomial tree, we first need…

You must be logged in to post a comment.