Excess Earnings (Residual Income) Valuation is an interesting approach to firm valuation, often commercialized by consulting companies because it can also serve as the foundation for management incentive systems.

At the initial stage, the method can be viewed as an Excess Cash Flow Valuation Model. That is, future cash flows can conceptually be divided into two parts:

- Cash flows whose discounting at the required rate exactly equals the value of the investment (i.e., NPV = 0), and

- The “excess” cash flows.

Accordingly, the first part can be recorded as the invested capital, and the second part as the present value of the excess cash flows (Excess FCF):

Mathematically, it can be demonstrated that this formula is equivalent to the standard DCF model.

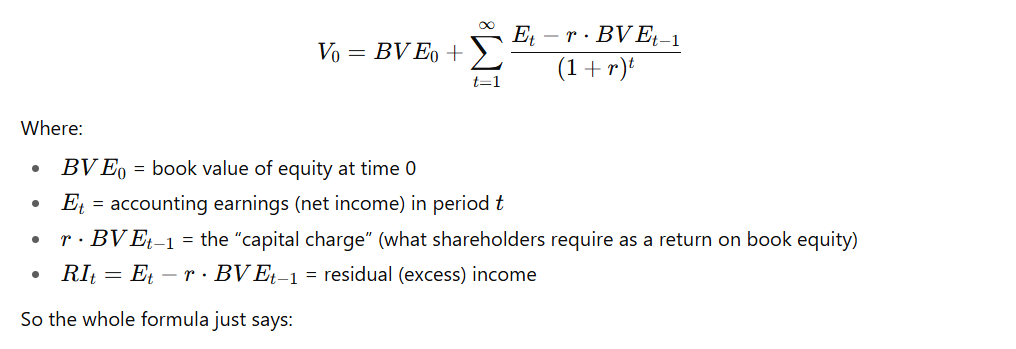

- If we take into account the algebra of deriving cash flows from the income statement and balance sheet items, the Excess Cash Flow formula can be transformed into the Excess Earnings formula (the algebra here is sufficiently complex). In the formula below, the assumption is that the firm is entirely equity-financed:

{kind=link}

P.S.

- This formula can also be reformulated into a two-stage model, just like in the standard DCF framework.

- The formula can be applied consistently within the WACC, APV, or Direct Equity approaches (just as DCF is).

- For the purpose of commercialization, consulting firms often adjust the accounting figures from the balance sheet and income statement in order to better define Economic Value Added (EVA) (see table). For example, R&D expenses may be capitalized and then amortized according to managerial judgment… Such accounting adjustments…

*Corporate Valuation Theory, Evidence and Practice

Mark E. Zmijewski; Robert W. Holthausen

Second Edition