Understanding the essence of options by a financier changes strategic decisions in management practice.

Another significant contribution of option valuation theories is the concept of real options, which, beyond tradeable options, allows specific numerical evaluation to inform decision-making.

One example is the option to expand a project, akin to a European Call option.

As financiers, we know that investing in a project with a negative NPV is a mistake. There might be potential for further expansion of the project at the next stage, but even then, the NPV from discounting future cash flows might still be negative.

Do you think it’s worth investing in such a project?

It depends on the circumstances.

The issue is that we consider the most likely scenario when forecasting cash flows. However, there might be, say, a 10% chance that the project’s NPV will be positive at the end of the first stage. In that case, we would invest in the second stage. If we are not lucky, we will abandon the continuation of the second stage.

Thus, we have an option where the exercise price is the investment needed for the second stage. The option’s value can be calculated by discounting the probable profit if successful, just as with standard tradeable options.

As a result, to make the right investment decision in the first stage, we must also consider the value of the option for the second stage.

[ PV = PV (1) + \text{Call Value (2)} ]

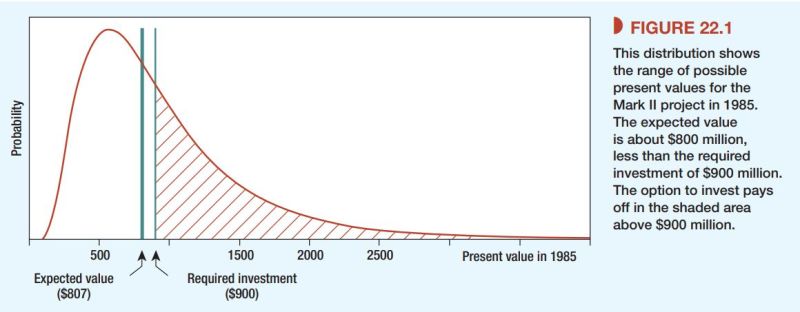

The photo below shows that the expected NPV of cash flows in the second stage is also negative, but the right tail indicates the range of the probability of success, which determines the option’s value.

Photo and insights from the book:

Principles of Corporate Finance – by F. Allen, R. A. Brealey, & S. Myers

You must be logged in to post a comment.