Corporate Valuation Theory, Evidence and Practice – by M. E. Zmijewski; R. W. Holthause

-

While Valuation, Excess assets should be separated from core operations and valued separately, but here it is important to see what effect this separation has on the right-hand side of the balance sheet when measured at market value… Does the removal of excess assets reduce debt, preferred stock, common equity, or other claims? The point…

-

In some cases, when valuing an organization, using the WACC method for discounting cash flows can be misleading, and it is better to use the APV method.To understand this, it is useful to look at the modified form of WACC, where it appears as a function of the value of the Interest Tax Shield (ITS).…

-

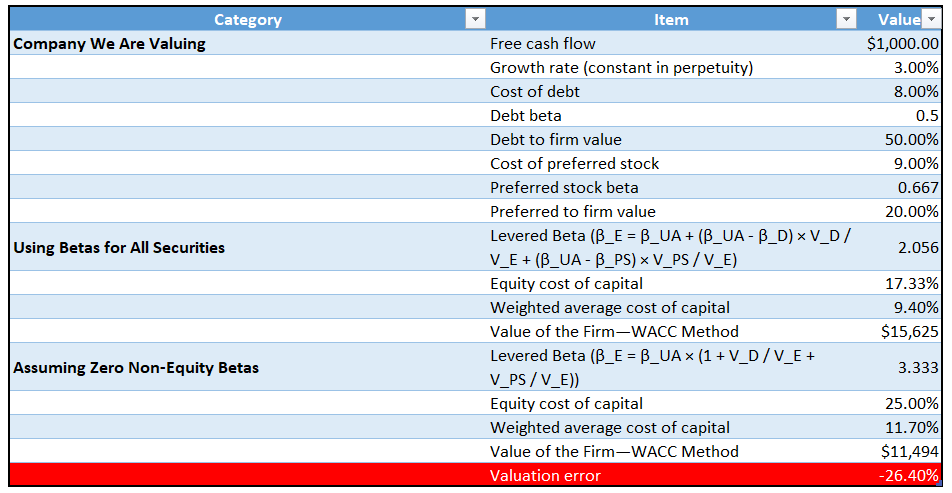

The table presents an example illustrating a widespread and significant error in valuation, related to the assumption of ignoring the beta coefficient of debt or other non-equity sources of financing—in this example, the error amounts to 38%. Source: Corporate Valuation: Theory, Evidence, and Practice, Mark E. Zmijewski; Robert W. Holthausen A common practical mistake is…

-

In the final sections, I want to address themes of capital valuation, where the formulas for financial “levers” and “revenues”, formulas you are familiar with, come into play. Now, I want to discuss those nuances which, in practice, distribute errors in the calculation of distress, default, and agency costs: These formulas consider the interest tax…

-

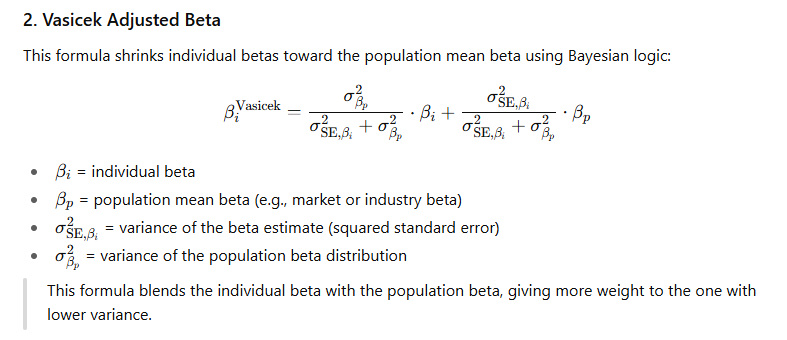

One reason for using comparable companies’ data to derive the beta of a listed company is that it yields a more accurate beta. Is it worth the effort? The issue is that when we obtain a company’s beta purely from statistical data, the resulting statistical beta has its own standard error, which is often quite…

-

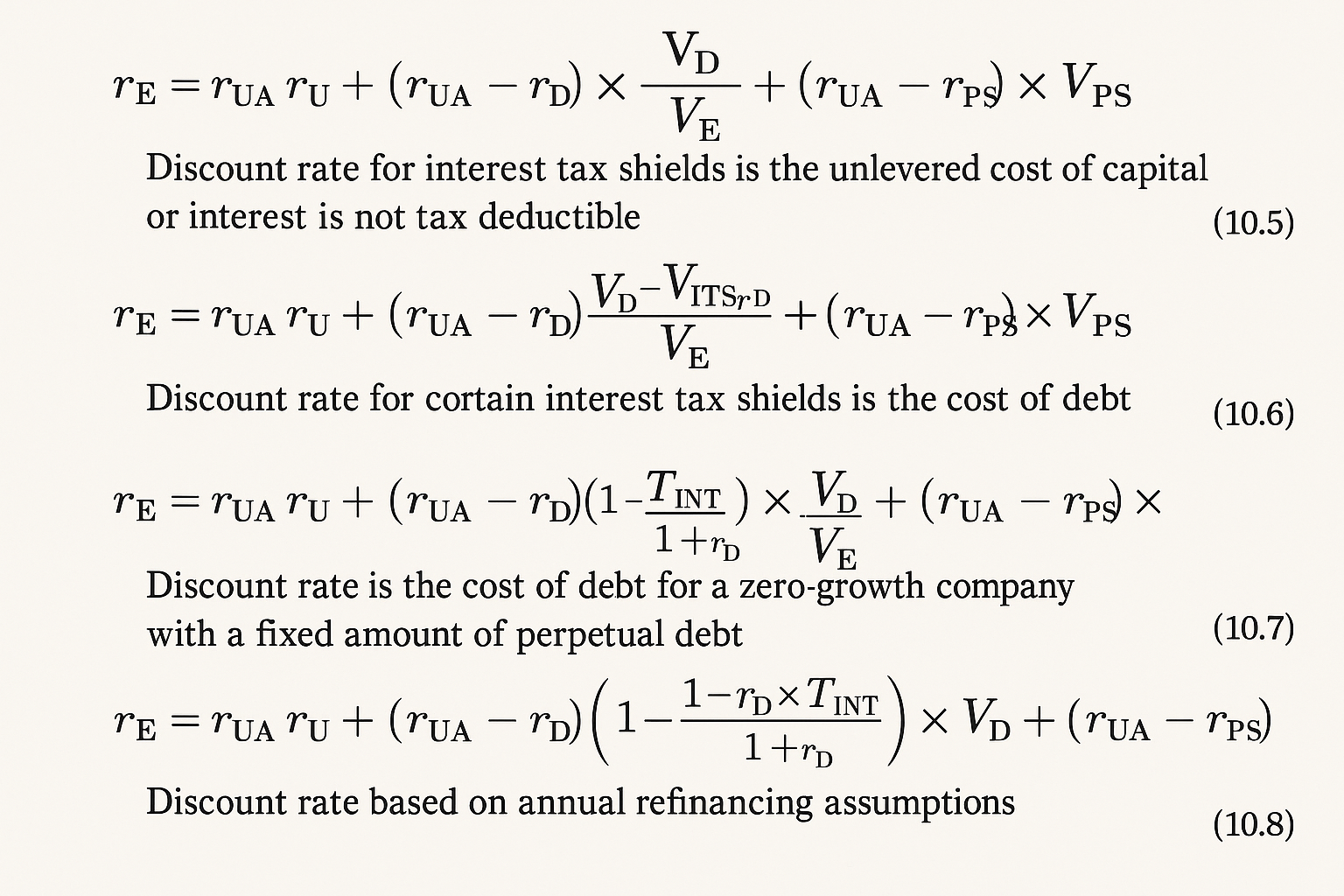

When valuing an organization, it’s easy to make mistakes if you approach the calculation of Cost of Equity and WACC superficially — because intrinsic value is highly sensitive to these parameters. In practice, the Unlever & Re-lever procedure is typically based on the following general formula derived from Modigliani–Miller (M&M) Proposition II with Taxes: However,…

-

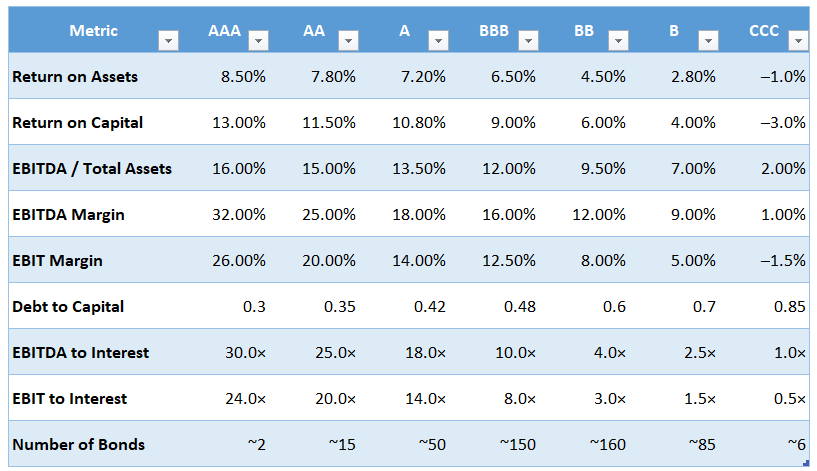

Among a CFO’s typical target KPIs is improving the company’s credit rating, as it directly impacts the organization’s value through its effect on the Cost of Debt (CoD) and ultimately the Weighted Average Cost of Capital (WACC). The CoD can be estimated using a modified version of the CAPM model. To do this, we need…

-

💬 How to Estimate Cost of Debt for Private Companies? For “listed” companies, the Cost of Debt (CoD) is more or less accessible. But how do we estimate this number when valuing a private company? Let’s say a company has a loan at 8% — can we just say its CoD is 8%?Or imagine the…

-

How to Calculate Expected Default Loss on a Bond? The cost of debt is often confused with the yield to maturity (YTM) of a bond/loan. The promised return is equal to the cost of debt when there is no risk of default. However, because there is a real risk of default, we must discount the…

-

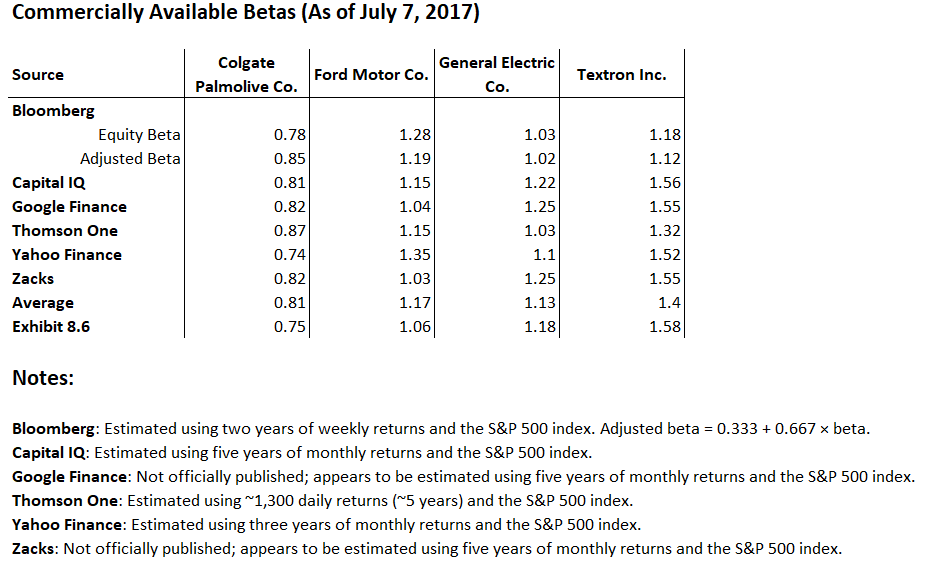

Adjusted β – It’s important to understand that statistical analysis provides an approximate rather than a “true” beta. Different commercial sources (as shown in the table) provide different data because they rely on different assumptions. The differences in assumptions pertain to the time frame over which beta is calculated (e.g., month) and the total period…

You must be logged in to post a comment.