- Consistency between numerator and denominator:

The numerator and denominator in the ratio must correspond. For example, Equity Value / EBIT is meaningless, because EBIT represents returns available to both equity holders and creditors. - Long-term operating results:

Both numerator and denominator should reflect long-term operating results. Temporary events should not distort the figures (Normalized Multiples). - Adjustments to financial statements:

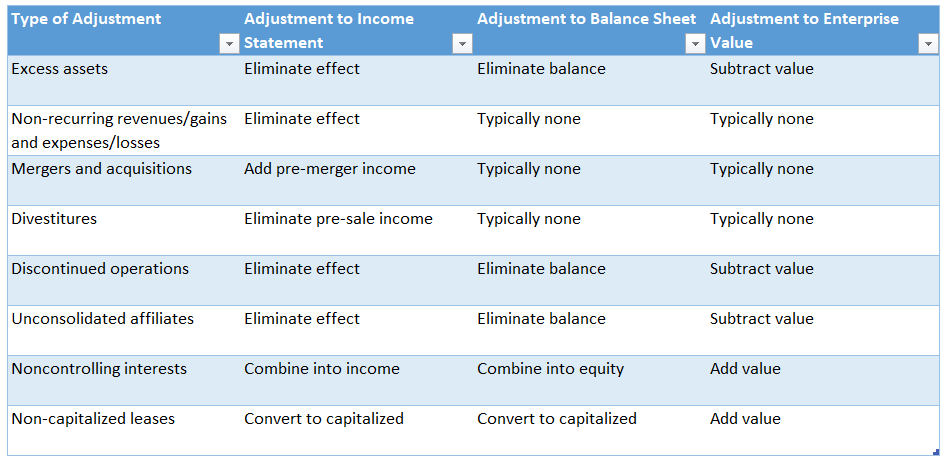

Financials must be adjusted to allow for apples-to-apples comparisons. Typical adjustments include (see table):- Excess assets – In some cases, the comparable company holds assets not essential to its core business. Such assets should be removed from the income statement, balance sheet, and cash flow statement. (Excess cash is also considered a non-operating asset, but since it is difficult to measure precisely, it is usually fully deducted in formulas.)

- Non-recurring items – One-time gains or losses not expected in the future should be eliminated.

- Mergers and acquisitions – When acquisitions occur, the acquired company’s assets and liabilities are consolidated on the balance sheet, but its full-year income will not be reflected in revenues. Therefore, pre-acquisition results should also be included in the metric.

- Divestitures – The opposite of M&A. Assets decrease, but the income statement still reflects results from the divested unit during the year. This must be adjusted.

- Discontinued operations – Sometimes a company plans to discontinue part of its activities. Under regulations, once such a decision is made, the results from discontinued operations must be reported separately.

- Unconsolidated affiliates – When a company owns less than 50% of another firm, its financials are not consolidated. In such cases, the asset and the cash flows generated from it should be separated when calculating multiples.

- Noncontrolling interests (minority interests) – When a company owns more than 50% of a subsidiary, full consolidation occurs, but equity includes a separate line for interests not owned by the parent. For multiples, the company should be treated as owning 100% of the subsidiary (except when the subsidiary operates in a different business segment with different risk characteristics).

- Leases – Operating lease contracts should be converted into finance leases. Leases must be treated as debt obligations.

*Corporate Valuation Theory, Evidence and Practice

Mark E. Zmijewski; Robert W. Holthausen

Second Edition

7 responses to “Key Adjustments in Applying Market Multiples”

[…] For comparisons, it is often also necessary to adjust the financial statements. You can find more details about this here: Key Adjustments in Applying Market Multiples. […]