If producing an iPhone in China costs $7 less on average, why not produce it in the US? The “mobility option” is a valuable asset that can be assessed thanks to modern financial science.

There are five strategic priorities that need to be balanced before starting factory construction: quality, cost, speed, environmental impact, and mobility. It’s clear that you can’t achieve all of these at once because they are often conflicting, but finding the right balance is possible.

The last one, mobility, becomes especially critical today. In the context of the production process, mobility can mean the ability to change production scales, the production product, and/or raw materials.

Increasing mobility naturally requires additional investment. Therefore, to make the right decision, it is necessary to evaluate the option in specific figures.

Let’s look at an example:

It is known that electricity production is more efficient with nuclear and coal plants than with gas turbines (combustion-turbine), but they are still built to meet peak demand because their operation and shutdown are relatively cheap and simple processes.

The profitability of such turbines depends on the difference between electricity prices and gas prices.

For most of the year, the operation of gas turbines is unprofitable, but there are periods when it becomes extremely profitable and justifies the investment.

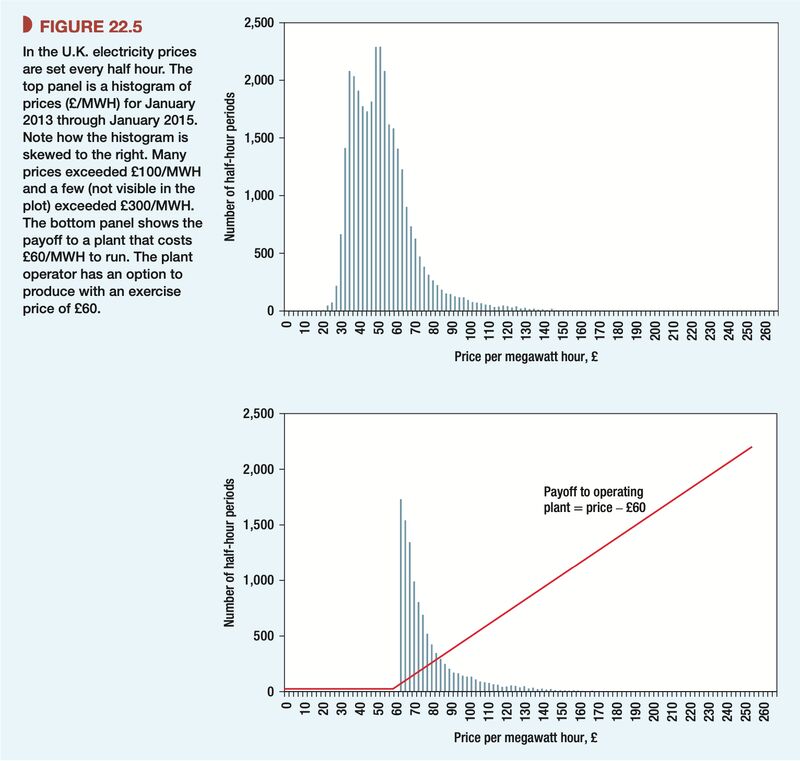

The histogram below shows the frequency of half-hour intervals of electricity prices in the UK in 2013-2014.

As you can see, the average price per MWh is below 60 pounds, and it is mainly less than 100 pounds, but there are rare cases when it exceeds 250 pounds.

Gas turbine profitability becomes positive above 60 pounds. The second graph shows the profitability achieved by turning on the turbine.

In essence, we are dealing with a series of consecutive half-hour Call options (you can turn it on and off), which can be calculated because we have statistical information about price fluctuations. The value of such plants is further increased by the fact that the plant can operate on oil as well as gas.

It should be noted that these graphs reflect a situation where gas prices are fixed; to get a more realistic picture, the graph should be built based on the statistical difference between electricity and gas prices.

P.S.

The advantage of factories in China lies in their ability to produce any smartphone in any quantity. If it turns out that demand has fallen, it’s not a problem; you reduce production. Doing this in the US is impossible because investments in mobility are very expensive. Increase mobility, and your production costs will skyrocket.

P.P.S.

With this note, I wanted to say that the “mobility option” is a very valuable asset for business, and its assessment is essential when making strategic decisions.

Photo and insights source:

Principles of Corporate Finance – by F. Allen, R. A. Brealey, & S. Myers