Implied Equity Risk Premium is a relative measure in finance that changes the investment philosophy and perspective…

Instead of assessing capital risk with historical figures, it’s possible to deduce from market observations a simple Gordon model (other versions exist – ROE, default spread, option volatility changes…).

Value = Div(1) / (r-g)

From this standpoint, understanding how dividends, stock prices, and expected growth rates change could lead to deducing what premium an investor demands from a given investment.

In a more sophisticated, and real version, integrating statistics of stock sales into the dividend part is possible… I won’t delve into the formulas, but if you’re more interested, you can find the professor’s thesis at this link:

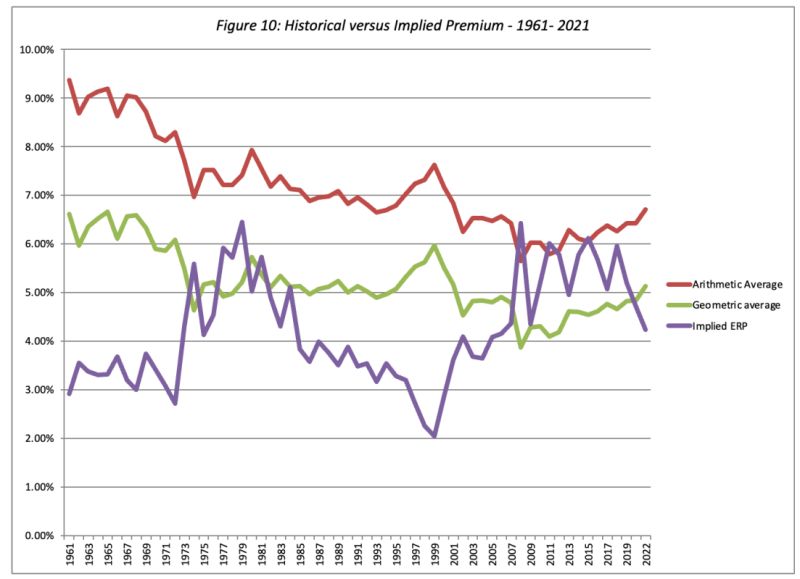

Here are some key points to consider:

- Differences between statistical and deduction-based figures can arise because historical statistics reflect real historical premiums, while deductions rely on market perceptions. For instance, when stock prices increase in a period, historical statistics show high premiums, but investors might be less cautious at that time, reducing the cost of risk…

- As “Implied” Premium suggests, it better anticipates the real premium of upcoming periods (with 76% correlation), compared to historical. Therefore, for better forward guidance, the use of Implied Risk Premium is a more rational decision;

- Using Implied Premium reduces the need for years of historical statistical analysis to minimize Standard Error. It works effectively even on short periods and provides a better opportunity for segmental and industry-specific analyses…

- From 2012 to 2021, the average Implied Equity Risk Premium in the US market was 5.35%*.

*Equity Risk Premiums (ERP): Determinants, Estimation, and Implications – The 2022 Edition Updated: March 23, 2022 Aswath Damodaran; Stern School of Business